Deepwater’s playbook for delivering growth

GORDON HARDIE and OBO IDORNIGIE, Welligence

Welligence recently participated in World Oil’s Deepwater Development Conference (DDC) in Lisbon, Portugal. DDC is a leading conference addressing technical issues related to engineering, development and production of oil and gas in deepwater and ultra-deepwater areas around the world. Welligence is the conference knowledge partner, and the conference was well-attended by oil companies, service providers, equipment manufacturers and other key stakeholders.

KEY TALKING POINTS

Some of the leading points addressed at DDC included the following:

- There was strong consensus at the conference that deepwater production remains a core part of the long-term energy supply mix. With supply disruptions from the Middle East, production from key deepwater hubs like Brazil, Gulf of America (GoM), Guyana and West Africa are becoming more critical to near-term supply.

- Welligence estimates that global oil production from deepwater fields is expected to ramp up from current levels of around 8 MMbpd to close to 10 MMbpd by the early 2030s. But to achieve this near-term growth trajectory, greenfield projects in Namibia, Brazil and West Africa with estimated capex of over $50 billion will need to progress in the short term.

- One of the main talking points at the conference focused on striking the right balance between innovation and standardization. While standardized hulls and equipment have helped shorten project cycle times, most notably with ExxonMobil in Guyana, it was also acknowledged that over-reliance on standardization can hinder the innovation cycle. Operators and contractors need to ensure that standardization does not come at the expense of technological progress.

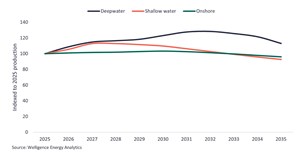

Fig. 1. Indexed global production outlook by sector, 2025-2035.

Fig. 1. Indexed global production outlook by sector, 2025-2035. - Deepwater production can offer some of the lowest-carbon barrels in an operator’s portfolio. The Equinor-operated Bacalhau development is the first FPSO to feature combined-cycle gas turbines targeting an emissions intensity of <10kgCO2e/boe, which is less than the deepwater average. But delivering these carbon efficiencies comes at a cost.

- The industry has traditionally prioritized capex efficiency and pace to first oil. But attention is shifting towards managing deepwater projects across the full production life cycle. Digital twins are gaining traction as an enabler for achieving this shift towards opex savings. With operators like bp and Shell deploying this technology on large-scale projects in the GoM, opex savings of around 10% to 20% are being touted. It remains to be seen if these projects can deliver these material gains.

DEEPWATER SECTOR REMAINS A CORE GROWTH ENGINE

Operators and contractors at the conference broadly agreed that deepwater projects will remain a growth engine for global oil supply. With the ongoing supply disruptions from the Middle East, production from deepwater hubs like Brazil, Guyana and West Africa are becoming ever-more-critical to global oil supply.

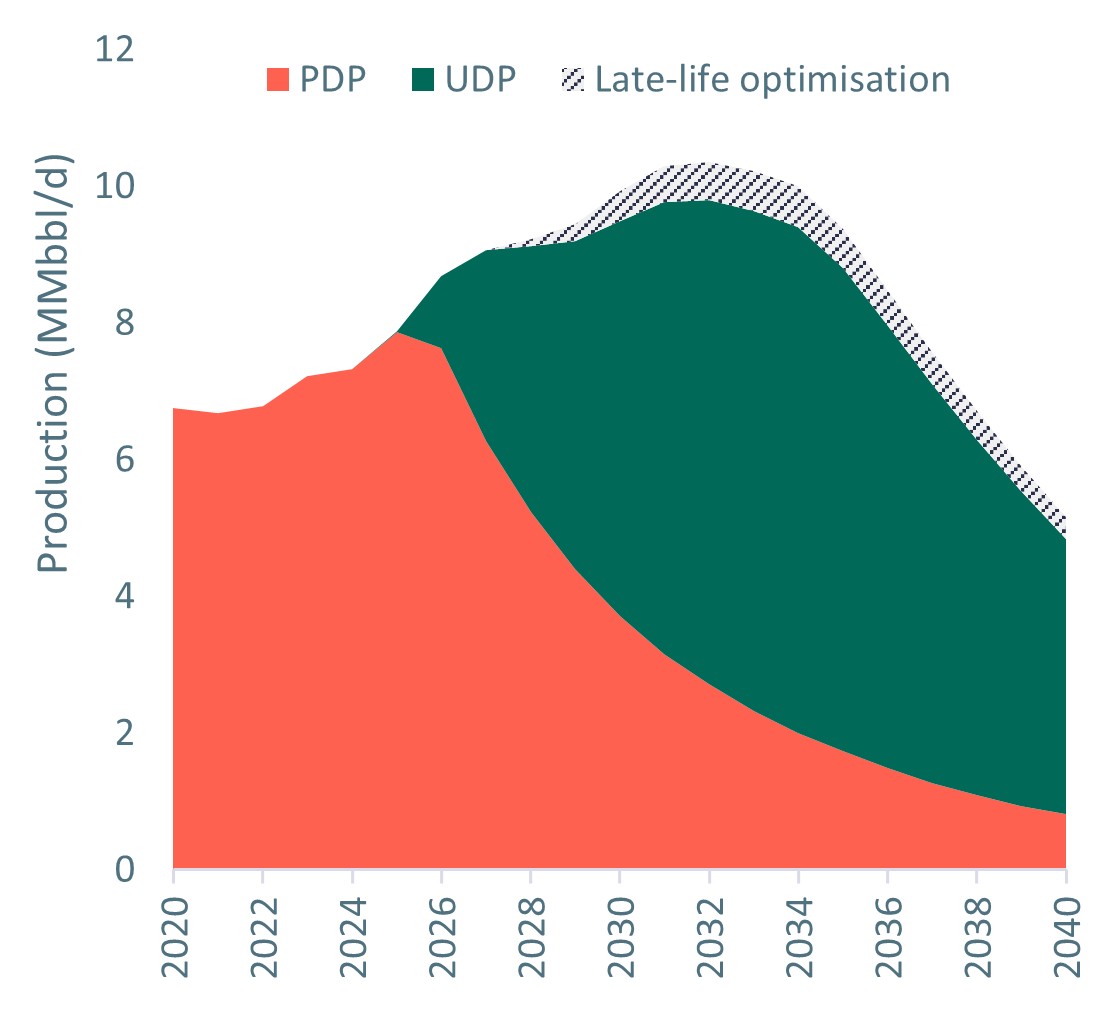

While production from conventional onshore and shallow-water assets is expected to remain broadly flat under our base case, Welligence estimates that global deepwater oil production will grow from its current level of around 8 MMbpd to close to 10 MMbpd by the early 2030s, Fig. 1. However, post-2035, deepwater production is set to enter decline unless the hopper of pre-FID deepwater projects is replenished in the medium-to-long term.

However, achieving this medium-term deepwater growth trajectory will require a tangible step up in investment. While over $200 billion in capex has been allocated to greenfield deepwater projects since the start of the decade, 2025 marked a notable low point—with only three standalone deepwater projects involving FPSOs reaching FID.

With IOCs maintaining a strong focus on capital discipline and increasingly selective around new investment, only the most resilient and commercially attractive deepwater projects are progressing to FID. A key theme at the conference was how operators can leverage new technologies and contracting solutions to reduce costs to improve project economics—ultimately unlocking the next wave of deepwater development.

STANDARDIZATION, INNOVATION AND THE CONTRACTOR CHALLENGE

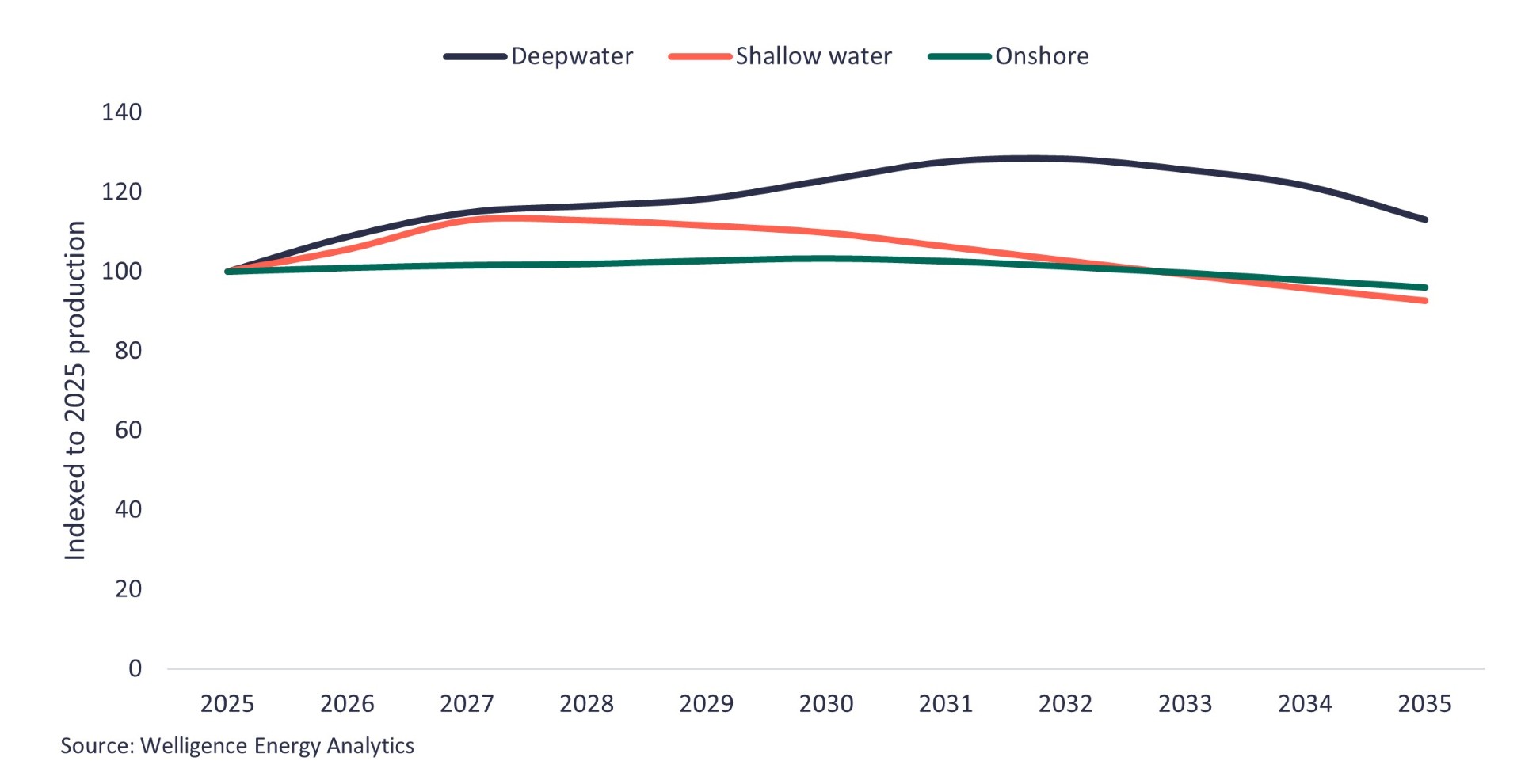

Standardization and its role in cutting project cycle times and costs was one of the key discussion points at the conference. However, there was also a concern that if standardization is not effectively implemented, it could hamper innovative solutions and limit competition.

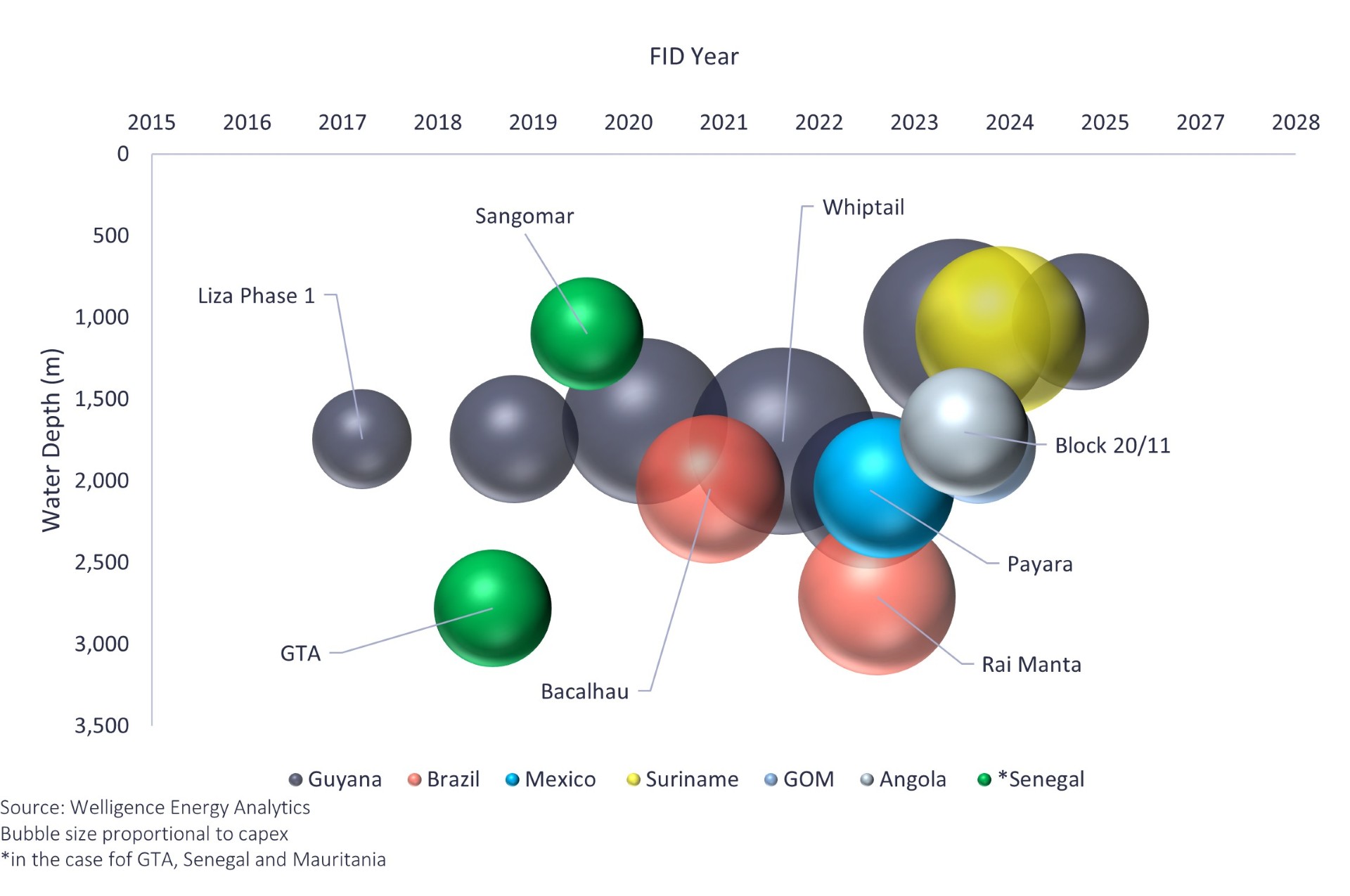

Welligence data highlight a clear correlation between improved project delivery and the deployment of standardized solutions, Fig. 2. Both the Payara and Yellowtail deepwater projects in Guyana are based on SBM Offshore's Fast4Ward standardized hull design and TechnipFMC's standardized subsea trees. Both projects were delivered ahead of schedule, a remarkable achievement for deepwater developments of this scale and complexity.

While the standardization approach has clear benefits in improving lead times and capital efficiency, the concern raised at the conference is that it should not come at the expense of innovation. A specific risk highlighted was that over-standardization could lock out other contractors from engaging with operators, ultimately reducing competition, breaking the innovation cycle and potentially limiting the introduction of new and more efficient solutions over time.

With the increased scrutiny on costs and project cycle times, we see operators preferring to lean towards the proven standardized solutions, particularly with regards to FPSO hulls and equipment, to deliver the next wave of projects.

CONSOLIDATION: A VALUE CREATOR OR A CONTENTIOUS DIRECTION?

Several IOCs are increasingly embracing the subsea iEPCI model (integrated engineering, procurement, construction and installation) , which drives stronger contractor engagement and collaboration during the early project phases. Projects such as Gato do Mato, Gran Morgu, and Bacalhau are all leveraging this approach, with schedule compression being the primary commercial driver. The merger of FMC Technologies, a subsea production specialist, with Technip, a leading SURF contractor, was key in enabling the iEPCI model. The proposed merger of Saipem and Subsea7 will also be looking to deliver integrated solutions.

While mergers like TechnipFMC reduce the interface and execution risk during the design and implementation phases, a contrary view is that it diminishes competition and risks stifling innovation at a time when new technologies are delivering meaningful project value.

EMISSIONS REDUCTIONS NOW EMBEDDED IN NEW PROJECTS: BUT AT WHAT COST?

A broader message from both operators and contractors was that emission reduction targets are not just aspirational statements but are now embedded as corporate KPIs. New developments are being assessed through a carbon lens as part of project screening, with emissions reductions being designed in, not just bolted on. However, while deepwater production can offer some of the lowest-carbon barrels in an operator’s portfolio, commercial viability is a challenge.

In the ultra-deep water of Brazil’s Santos basin, the Equinor-operated Bacalhau FPSO is the first to feature combined-cycle gas turbines. The technology generates more power using the same amount of gas, increasing energy efficiency and reducing CO2 emissions. While forecast emissions are set to be more than half that of the industry average, the topside weight requirement (around 50,000 tonnes) is a lot heavier than the conventional FPSO with processing capacity of over 150,000 bpd (average topside weight of 30,000 to 40,000 tonnes), Fig. 3. With FPSO topside costs estimated to cost around $50,000 and $60,000 per tonne, the incremental capital required can be in the hundreds of millions of dollars.

Another low-emission FPSO technology is the all-electric concept. Petrobras’ P-84 and P-85 FPSOs, currently under construction, are based on this solution. The estimated costs for each FPSO at FID will be $4.1 billion (which is almost double the cost of the P-83 FPSO sanctioned two years earlier), Fig. 4.

During the conference, several sessions focused on new, innovative technologies that, if implemented from the onset, could make a material difference to the life of field emissions profile of an asset. One of the emerging technologies involves moving the subsea processing equipment to subsea, which could ultimately reduce the operational footprint on the FPSO topsides. This solution could lead to overall reduction in emissions, while at the same time also cutting the topside weight requirement for the FPSO. But the potential costs and system reliability will be critical to adoption.

DESIGNING FOR LATE-LIFE OPERATIONS CAN OFFER LONG-TERM OPEX SAVINGS

With late-life operations come integrity challenges, equipment reliability concerns and processing constraints. As the onstream batch of global deepwater projects matures–over 30 deepwater assets have been producing for over 25 years–life extension has become increasingly central to operator strategies. Designing for late life is now critical for long-term opex reduction, especially as decisions made at the early stages of a development will adversely impact the cost of operating an asset across its full lifecycle, Fig. 5. But the recent trend has focused on disciplined capital spending, fast track and standardization.

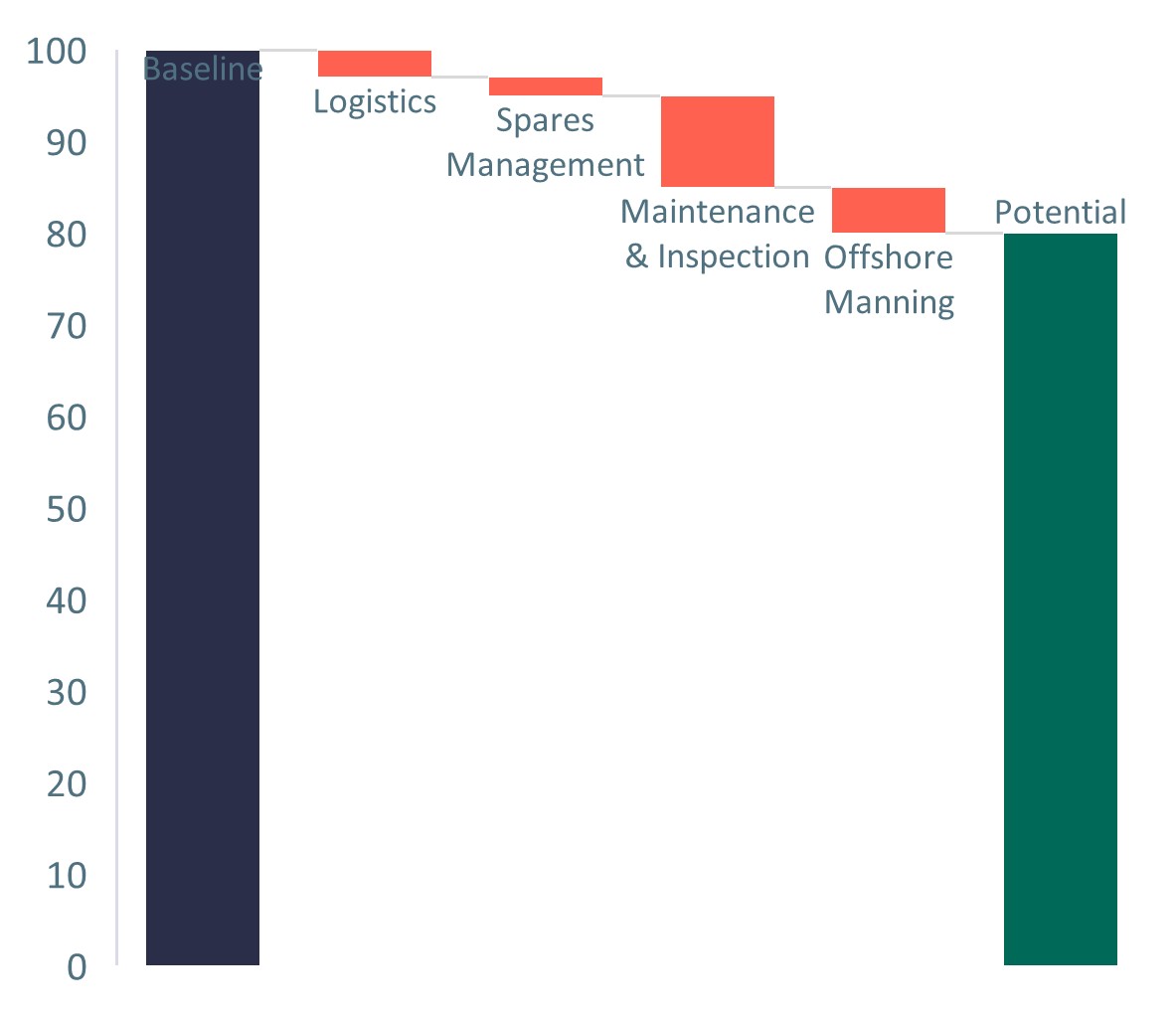

The conference highlighted a growing comfort with new technology, especially digitization and artificial intelligence (AI), where adoption of technologies like digital twins can be leveraged for real-time monitoring to provide early risk identification, Fig. 6. With predictive analytics, operators can pre-emptively intervene rather than reactively fix. This new approach reduces the process downtime by up to 30% in some deployments. AI can also streamline and eliminate waste. Logistics, spares management, optimized maintenance and inspection routines and reduced specialist interventions can significantly reduce opex. Savings of between 10% and 20% have been projected. With early adoption by operators, including bp and Shell in the GoM, the industry will be watching closely to see if these projects can deliver these material savings.

The overarching message from the conference was that the industry has tended to optimize capex spend and delivery of first oil, often at the expense of the decades that follow. As companies push the deepwater envelope and projects become increasingly more challenging, designing systems for remote operations, not only reduces safety risk, but can materially reduce the cost of crewed interventions over field life. While high initial costs have muted early implementation, with continual improvement in data processing and AI, tangible savings are likely and with that, a new addition to the deepwater playbook.

For questions or more information on Welligence products, please contact us at info@welligence.com.

GORDON HARDIE joined Welligence in March 2025 and currently leads the Sub-Saharan Africa Research team. He is responsible for the team’s regional coverage, promoting thought leadership reports, investment/M&A trends and key producing country analysis. Prior to Welligence, Mr. Hardie spent over 15 years in various upstream petroleum engineering roles, working for Talisman Energy, Repsol-Sinopec and most recently Apache North Sea. He holds a master’s degree in petroleum engineering from Heriot-Watt University and an MBA from the University of Edinburgh.

OBO IDORNIGIE is senior vice president, Energy Trends & Analytics, at Welligence. Prior to joining Welligence, he spent 12 years with Wood Mackenzie as an Africa-focused analyst and later as a corporate analyst. Mr. Idornigie had previously worked for two years with the Nigerian government. He has authored reports on issues relating to gas monetization in West Africa, the outlook for the offshore facilities market, and benchmarking fiscal terms in West Africa. Mr. Idornigie holds a BSc (Hons) degree in geology and mining from the University of Jos, Nigeria, and an MSc degree in oil and gas economics from the University of Dundee, Scotland.

Related Articles- Unlocking ultra-high-pressure reserves: Why Shenandoah is a milestone for deepwater engineering and advanced chemistry (March)

- First Oil: Our Deepwater Development Conference rides the sector’s momentum (March)

- FPSOs, reliability and gas turbine air intake filtration (February)

- Engineering for the deep: Human support and rescue systems (November 2025)

- Full-scale test rig validates benefits of electric BOP (August 2025)

- Powering Mero-3: A look inside one of the world’s largest deepwater FPSOs (August 2025)

- Subsea technology- Corrosion monitoring: From failure to success (February 2024)

- Applying ultra-deep LWD resistivity technology successfully in a SAGD operation (May 2019)

- Adoption of wireless intelligent completions advances (May 2019)

- Majors double down as takeaway crunch eases (April 2019)

- What’s new in well logging and formation evaluation (April 2019)

- Qualification of a 20,000-psi subsea BOP: A collaborative approach (February 2019)