Management issues: Recent O&G survey reveals increased interest in financing new wells

In October, Haynes and Boone, LLP released its fall 2023 Borrowing Base Redeterminations Survey, which showed an increased interest in financing new development oil and gas wells but a tight reserve-based lending (RBL) market. Respondents also don’t expect meaningful borrowing base increases this determination season, despite favorable oil and natural gas prices.

An RBL financing is structured as a revolving loan with credit availability, based on the value of an upstream producer’s oil and gas reserves.

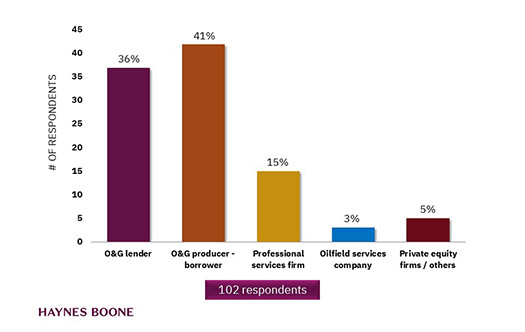

Haynes Boone conducted the survey following a third-quarter run-up in commodity prices driven by strong global demand for oil and natural gas, as well as conflict in the Middle East. This is the firm’s 18th semi-annual borrowing base redeterminations survey since 2015 and includes input from more than 100 executives at oil and gas producers, financial institutions, private equity firms and professional services firms, Fig. 1.

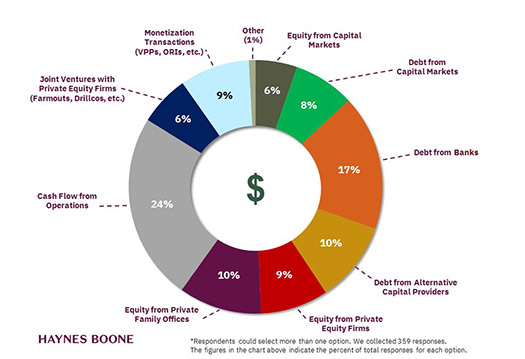

The key findings include an expected meaningful decrease in using commercial bank RBL capital as a financing source next year. Instead, industry executives expect to use equity and debt from capital markets more in 2024 than in prior years, Fig. 2. From spring to fall of this year, expectations of use of debt capital markets increased from 5% to 8% and equity capital markets tripled from 2% to 6%. Although the mix of external capital sources has changed over the last several surveys, an internal capital source—cash flow from operations—remains the most popular source of funding.

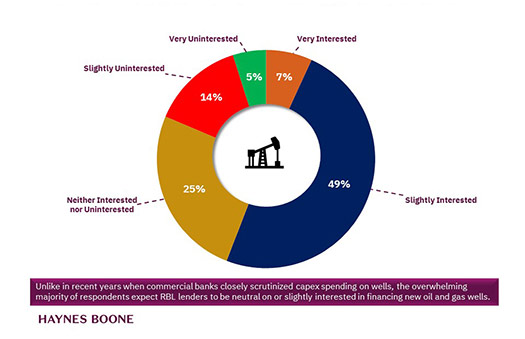

Despite a tepid RBL market, there is a change in interest from RBL lenders to finance new drilling programs, Fig. 3. A strong plurality, 49%, of respondents said RBL lenders were “slightly interested” in funding new drilling, and 7% said lenders were “very interested,” with 25% believing lenders were neutral.

Volatility continues to be a common word in any oil and gas industry call, and there’s no sign of that fading soon. Our most interesting finding may be that despite lingering RBL market pessimism, participants in the RBL financing market are showing new interest in funding drilling and completion programs, which is a change from prior years, where lenders closely scrutinized developmental capital expenditures.

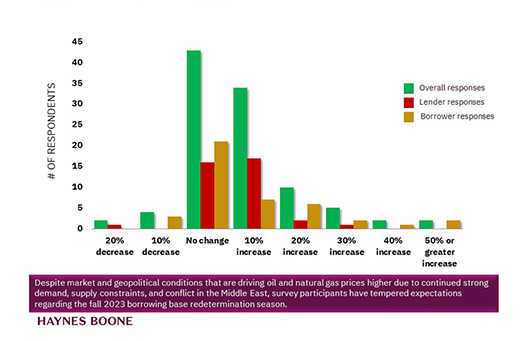

Despite recent increases in oil and natural gas prices, about 35% of survey respondents expect only a 10% increase in borrowing bases this fall and just over 40% expect no change at all, Fig. 4.

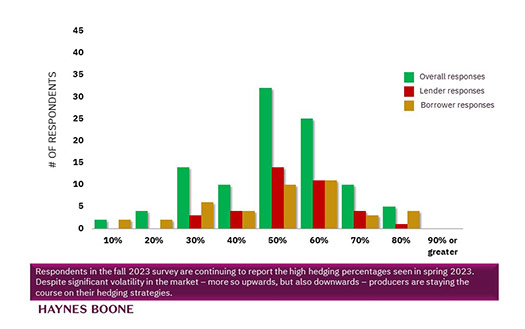

Another element unlikely to change is the increased hedging percentages that first popped up in the spring of this year. About a third of survey participants expect borrowers to hedge 50% of future production for the next 12 months, and around a quarter of respondents expect a 60% hedge of production, Fig. 5.

Haynes Boone’s Energy Practice Group manages high-stakes transactions and litigation, as well as financings, restructurings and regulatory advice for a diverse array of clients in the U.S. and overseas. Lawyers in the group closely follow industry developments and regularly prepare useful reports for industry participants including borrowers, lenders, private equity firms, investment funds, and others.

- Dallas Fed: Outlook improves, even as activity little changed; break-even prices increase (April 2024)

- The last barrel (February 2024)

- Oil and gas in the Capitals (February 2024)

- What's new in production (February 2024)

- First oil (February 2024)

- E&P outside the U.S. maintains a disciplined pace (February 2024)

- Applying ultra-deep LWD resistivity technology successfully in a SAGD operation (May 2019)

- Adoption of wireless intelligent completions advances (May 2019)

- Majors double down as takeaway crunch eases (April 2019)

- What’s new in well logging and formation evaluation (April 2019)

- Qualification of a 20,000-psi subsea BOP: A collaborative approach (February 2019)

- ConocoPhillips’ Greg Leveille sees rapid trajectory of technical advancement continuing (February 2019)