Shaletech: Permian Basin

The transcendental Permian basin of West Texas and southeastern New Mexico shows no signs of relinquishing its position as ground zero in the unconventional sector’s guarded transition from survival to growth mode. Recent statistics speak for themselves:

Eight operators combined have shelled out nearly $22 billion of late to snatch up assets in a play where per-acre price tags are approaching $60,000. Three midstream acquisitions, this year alone, add another $4.68 billion to the regional investment mix.

Nearly 40% of all active U.S. land rigs are at work in the Permian’s Midland, Delaware and Northwest Shelf sub-basins, with five rigs on average joining the local fleet every week since the first of the year.

The horizontal drilling permits that Texas issued in the first quarter of 2017 equals more than 41% of all the permits authorized last year.

Estimated oil production stands at more than 2.3 MMbpd, compared to just under 2.7 MMbpd for the Eagle Ford, Bakken and Niobrara shales combined. For perspective, Saudi Arabia’s Ghawar complex, by far the world’s largest conventional oil field, reportedly produces at a 5.0-MMbpd clip.

“The Permian basin will clearly be the driver of strong growth in the second half of 2017 through 2018 and well into the future,” Apache Corp. President and CEO John Christmann told investors in early March. Apache created a buzz last September with the announced discovery of the Alpine High resource play in a largely undeveloped swath of the southern Delaware basin (Fig. 1), where it is spending $500 million to build a natural gas liquids (NGL) infrastructure with the first major sales line connection on tap for a July start-up.

Christmann echoes most of his peers, who despite the likelihood of continued price volatility and nagging takeaway and associated discounting issues, see this high-return and multi-pay zone juggernaut as providing a long-awaited lift to lagging bottom lines. The same for the drilling contractors and service companies lying-in-wait to recoup some of the cost concessions extended over the past couple of years.

“We actually believe that if oil stays kind of range-bound between $50 and $55, the impetus behind service cost increases will be muted a little bit,” Diamondback Energy Inc. CEO Travis D. Stice said in February. “However, if we continue to see commodity prices strengthen to $55 to $60 a barrel, we believe you’ll see these service cost increases start to accelerate in the back half of this year.”

‘PERMI-PASSION’ HEATS UP

The Permian basin active rig count has risen every week since the first of the year, from 267 on Jan. 6 to an April average of 338, more than double the 140-rig average for April 2016, according to Baker Hughes, which recorded a 12-rig jump between March 31 and April 7.

Correspondingly, the horizontal drilling permits that the Texas Railroad Commission (RRC), the state’s chief regulator, issued in the first quarter likewise have more than doubled from the same three-month period of 2016. The agency’s database shows 1,624 horizontal permits authorized in the three applicable RRC districts (8, 8A, 7C) over the first quarter this year, compared to 712 new well authorizations for the first quarter of 2016. The agency approved a cumulative 3,929 Permian drilling permits last year for all wellbore profiles.

By contrast, the RRC’s cross-state sister agency, the New Mexico Oil Conservation Division (OCD), approved only 44 drilling permits between Jan. 1–April 18 in the three counties (Eddy, Chaves and Lea) that comprise the state’s Delaware basin fairway. A dissection of OCD data shows 125 drilling permits authorized in the three counties for all of 2016.

As for oil production, the latest best guesstimate from the U.S. Energy Information Administration (EIA) shows an estimated 2.362 MMbpd being produced in the two-state Permian region in May, a 76,000-boed jump from April (Fig. 2). The EIA pegs May gas production at 8,135 MMcfd, a projected 159-MMcfd increase, month-on-month. In March, the last month in which data are available, the EIA also shows the Permian with a nation-high inventory of 1,864 drilled-but-uncompleted (DUC) wells.

One of the key Permian differentiators is the geological stacking of up to 12 different pay zones, putting less weight on the aerial reach of an operator’s leasehold than plays with fewer prospective horizons. “The issue in the Permian basin is that everywhere we look, and as we look deeper, we find more opportunities,” said Occidental Petroleum Corp. President and CEO Vicki Hollub.

After adding two rigs in January, Occidental plans to run between six to eight rigs this year, with 26 new wells planned for the first quarter. Occidental holds 2.5 million new acres in the Permian, of which 1.4 million acres comprise its unconventional resource base.

CONTEMPORARY LAND RUSH

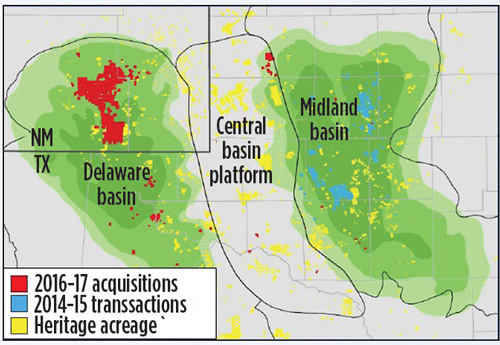

Atypical of most unconventional plays, super-majors hold prominent roles in the Permian, as reinforced on Jan. 17, when Exxon Mobil Corp. increased its Permian stake with the $6.6-billion acquisition of over 227,000 net acres in the New Mexico Delaware basin, once controlled by the storied Bass family of Fort Worth, Texas. The newly acquired Delaware basin acreage holds an estimated 3.4 Bboe, recoverable “from multiple stacked pay zones,” which Exxon Mobil says will double its Permian resource base, Fig. 3.

“The holdings are highly contiguous, and leveraging Exxon Mobil’s technology and operating experience, we will drill some of the longest wells in the Permian, reducing development costs and increasing reserve capture,” Chairman and CEO Darren Woods told analysts on March 1. “The majority of the wells in the Delaware basin will have lateral sections between 10,000 and 12,500 ft.”

Through its XTO Energy subsidiary, Exxon Mobil was running 10 rigs prior to the acquisition and reportedly plans to steadily increase to 25 rigs.

Noble EnergyInc. kicked off the 2017 land grab with the $2.7-billion acquisition of regional producer, Clayton Williams Energy, on Jan. 16. Assets acquired in the transaction, which closed on April 25, include 120,000 net acres and an estimated 2 Bboe reserves in the southern Delaware basin, much of which is contiguous with Noble’s existing 47,200-net-acre Texas leasehold in Reeves and Ward counties.

Noble plans to run six rigs and drill around 55 wells this year, primarily targeting the upper and lower Wolfcamp A.

In February, pure play operator Parsley EnergyInc. unwrapped its $2.8-billion purchase of 71,000 net acres of undeveloped and producing acreage in the Midland basin, formerly controlled by Double Eagle Energy Permian LLC. Upon closing, the company will hold 227,000 net acres.

Parsley started 2017 with 10 active rigs. The firm plans to add four rigs and to complete between 120 and 140 horizontal wells by the end of the year, primarily targeting the Lower Sprayberry, Wolfcamp A and Wolfcamp B horizons.

With the Feb. 28 closing of its $2.55-billion acquisition of Brigham Resources, Diamondback Energy now holds more than 186,000 net acres across the Midland and Delaware basins. The deal included over 80,000 net acres, and roughly $50 million in midstream assets in Pecos and Reeves counties of Texas.

Diamondback, which is running eight rigs and three frac spreads, expects to complete between 130 and 165 gross wells this year, at average lateral lengths of 8,500 ft, primarily focusing on the Wolfcamp A.

On March 21, Marathon Oil acquired approximately 21,000 net acres in the northern Delaware basin of New Mexico from Black Mountain Oil & Gas and other private sellers for $700 million. Marathon, which now controls 90,000 net acres, says its northern Delaware assets have nearly 5,000 ft of stacked pay from up to 10 target benches, delivering more than 90% returns at a flat $55/bbl oil price. The company plans to be operating three rigs by mid-year.

Meanwhile, the Permian basin was a veritable shopping mart last September and October, with EOG Resources, RSP Permian and Concho Resources inking separate deals worth nearly $7 billion.

EOG was the high roller with its September $2.5 billion bolt-on acquisition of Yates Petroleum Corp., the largest deal in the company’s history. The purchase gives EOG another 186,000 net acres of Wolfcamp, Bone Spring and Leonard shale stacked pay in the New Mexico Delaware basin, as well as 138,000 net acres on the Northwest Shelf. The company holds a combined 574,000-net-acre position, where it plans to operate 11 rigs in 2017, to drill upwards of 140 largely Wolfcamp wells.

With its $2.4-billion buy-out of Silver Hill Energy Partners on Oct. 13, RSP Permian now holds around 47,000 net acres in the Midland and Delaware basins. As of March 27, RSP was operating six rigs and plans to exit 2017 with an eight-rig fleet. RSP’s comparably modest leasehold closed out 2016 with full-year production of 29,200 boed.

Concho’s $1.625-billion acquisition of Reliance Energy’s Midland basin assets on Oct. 6 added 40,000 net acres, expanding its property base to 930,000 gross (600,000 net) acres. Located in Andrews, Martin and Ector counties of Texas, the acquired assets include 10 MMboed of production.

Concho was running 21 rigs in February and said 40% of its $1.6–$1.8 billion 2017 capital budget will be diverted to the northern Delaware basin, where it will average eight operated rigs. As of March, Concho also plans to run an aggregate nine rigs in the southern Delaware and Midland basins, drilling wells with average lateral lengths of 10,000 ft. Two rigs are devoted to the Northwest Shelf.

BHP Billiton and others, however, are foregoing high-dollar acquisitions in favor of straightforward asset swaps to contiguously expand leaseholds, largely to accommodate longer laterals. “We have been successful in swapping approximately 4,000 net acres with other operators in the area to build contiguous sections that are enabling us to drill longer laterals and, therefore, get higher returns,” says Alex Archila, BHP asset president, shale.

As of Jan. 25, BHP Billiton was operating a single rig for lease retention and running additional tests aimed at optimizing the development of roughly 78,000 net acres in its core Reeves County leasehold. “We now have a clear line of sight to a 150,000-boed business in net terms, based on a six-rig program, targeting the sequential development of the Upper, Middle and Lower Wolfcamp horizons,” Archila said.

FEVERISH PACE

In its sidetrack to short-cycle, high-payout projects, Chevron is ramping up activity in its legacy 1.5-million-acre Midland and Delaware properties, where it has established a minimum $2-billion budget this year. After ending 2016 with 15 operated and non-operated rigs, Chevron aims to be running 15 operated rigs by year end “with more on the non-operated side,” building up to an operated 20-rig fleet by the end of 2018.

Chevron says its current guidance calls for production of 325,000 to 450,000 bopd through 2020. Owing to numerous prospective landing zones, the major says its surface assets correlate to 11 million “bench acres,” boosting upside potential for production of more than 700,000 boed within a decade.

While providing no specifics, Shell says more than half of the $2 billion to $3 billion earmarked for shale development this year will be directed to the Permian basin, followed by its Canadian Duvernay holdings. At last report, Shell and Anadarko PetroleumCorp. remained in negotiations to decide what to do with their 10-year-old joint venture, set to expire this summer, covering 350,000 acres in the Delaware basin.

For its part, Anadarko wrapped up 2016 with 14 operated rigs and three completion crews within its 580,000-gross-acre leasehold in the Texas Delaware basin, prospective for the four-bench Wolfcamp, the Avalon and the Bone Springs shales. Anadarko, which put 78 wells online last year and delivered record fourth-quarter production of 50,500 boed, plans to operate 10 to 14 rigs during 2017 and drill more than 150 mid-lateral-equivalent wells.

A sampling of fellow independents, likewise, shows the resurgence is well underway. Apache, for one, plans to divert upwards of $2 billion this year to the 3.1 million gross acres it holds in the Midland and Delaware basins. The Houston-based independent plans to run at least 11 rigs in 2017, including four to six rigs and two frac crews dedicated to Alpine High in southern Reeves County, Texas, where as of March 27, 16 NGL wells were shut in, awaiting infrastructure completion. On Feb. 23, Apache’s Christmann said reports of preliminary flowrates not living up to expectations are unfounded. “I know there was a little bit of a negative reaction to some of the rates, because everybody’s expecting us to be optimizing and scaling-up our fracs and things, but we’re very pleased with where we are, and the scope and scale of this field has done nothing but get bigger since our initial disclosure in September of last year,” he said.

Encana Corp. is running five rigs in its 127,000-net-acre Midland basin leasehold, including four dedicated to its RAB Davidson pad (Fig. 4), where 14 wells went on production last year. Once the 19 wells now being drilled are completed, the pad will comprise 33 producing wells, representing what Encana says is the basin’s first full-scale, high-density development across multiple stack zones in the Sprayberry, Wolfcamp A and Wolfcamp B formations. Encana’s 2017 guidance calls for drilling 135 to 145 net horizontal wells at an estimated total cost of $5 million/well, normalized for average 8,100-ft laterals.

Devon EnergyCorp. is squarely in growth mode on the 650,000 net acres it controls in the Texas and New Mexico Delaware basin, where it will drill at least 100 wells principally targeting the Wolfcamp and Leonard shales. “With an improving cash flow stream, we are planning to steadily ramp up drilling activity throughout the year, to as many as 20 operated drilling rigs by the end of 2017, roughly doubling our rig count from year-end 2016,” President and CEO Dave Hager said in February.

Pioneer Natural Resources Co. plans to return to year-end 2015 form, with 18 rigs across its 825,000-net-acre Midland basin asset. Four of the rigs will be dedicated to the Southern Wolfcamp joint venture with China’s Sinochem. Pioneer plans to put 260 Sprayberry/Wolfcamp wells on production, largely employing its now-standard upsized completions, and where leases so allow, longer laterals. “Our preference is to drill 10,000-ft laterals, but there are times when the lease configuration limits us to approximately 7,500-ft laterals. This is where the larger completions could make a lot of sense going forward,” says President and COO Tim Dove.

EP EnergyCorp., which owns 178,000 net acres in the Midland basin, on Jan. 26 signed a joint venture agreement with private capital investor Wolfcamp Drillco Operating L.P. that provides for drilling up to 150 wells in two 75-well tranches. EP, which is operating five rigs and two Wolfcamp-directed frac crews, plans to complete 90 to 105 wells this year.

Cimarex EnergyCo. also looks to repeat 2015 with 60 wells planned for completion, double the wells completed in 2016. Cimarex is operating 11 rigs and looks to expand to 18 by year-end across its 190,000-net-acre position, which includes 100,000 acres dedicated to the Chevron Wolfcamp joint venture in the Culberson, Texas area. There, Lower Wolfcamp wells are being drilled with 10,000-ft laterals and completed in 48 stages with 2,400 lb/ft proppant loads.

TAKEAWAY CONCERNS

Escalating production of oil and associated NGLs threatens to soon overwhelm existing pipeline and gathering capacities. So say Bloomberg analysts, who projected on March 31 that Permian oil production could reach 2.65 MMbpd by December, while year-end takeaway capacity will be limited to 2.54 MMbpd.

The expected demand has spurred plans for at least two major newbuild networks and a trio of significant midstream acquisitions, the latest coming on April 18 with private equity firm Blackstone’s announced $2-billion acquisition of Eagle-Claw Midstream Ventures. The deal would include 375 mi of gas pipeline and processing facilities in the Delaware basin.

NuStar Energy is expecting a May closing on its $1.48-billion buyout of Navigator Energy Services, which would give the midstream operator a 500-mi oil pipeline in the Midland basin with 74,000-bpd carrying capacity. The transaction also included a gathering system and some 1 million bbl of storage capacity.

On Jan. 24, Plains All American said it would pay $1.2 billion to acquire southeastern New Mexico’s 515-mi Alpha Crude Connector pipeline and associated gathering and storage system from co-owners Concho Resources and private equity firm Energy Spectrum Capital. The newly acquired network will connect with the to-be-expanded BridgeTex and Cactus pipeline systems that terminate near Houston and Corpus Christi, respectively. Takeaway capacity is expected to be increased to 400,000 bopd from the current 300,000 bopd.

In related developments, Enterprise Products Partners and Kinder Morgan separately announced plans for two new Permian pipeline networks, both planned for 2019 completion. On April 10, Enterprise unveiled its intention to build the 571-mi Shin Oak NGL pipeline to Houston, with initial capacity of 250,000 boed. While not disclosing capacities, Kinder Morgan on March 22 laid out plans for a new build 430-mi gas pipeline, terminating at Corpus Christi. ![]()

Leave the Fusion to Nuclear Energy:

Saving Time with Grooved Technology

for Permian Water Disposal Facility Construction

Hydraulic fracturing and horizontal drilling have allowed the oil and gas industry to unlock significant oil and gas resources in the Permian basin. But along with the valuable hydrocarbons comes a challenge: huge volumes of produced water that must be managed and disposed.

Produced water transportation and disposal costs pose the biggest challenge to Permian basin shale producers’ financial bottom lines. According to IHS-Markit, produced water management can represent half of a shale well’s operating expenses and these costs will rise as focus shifts to growth. To put a lid on these inflating costs, some producers are building their own production and water disposal facilities, instead of relying on third-party waste management companies.

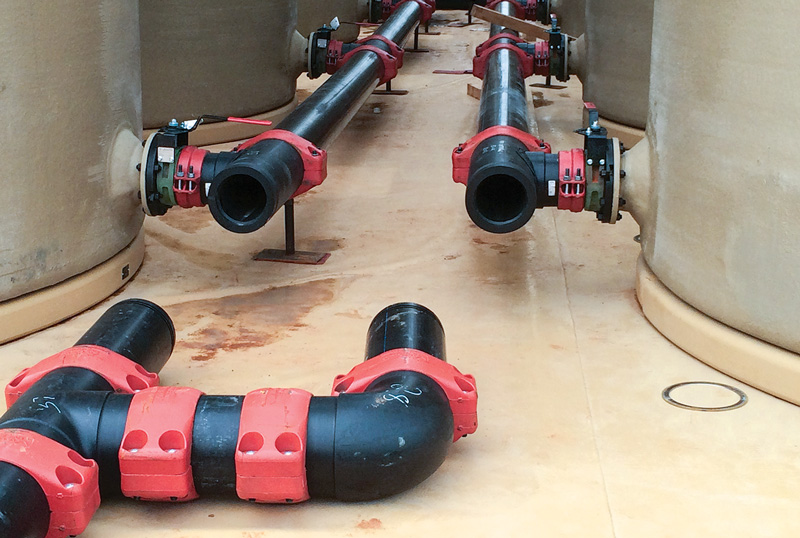

One of the largest acreage holders in the Permian has found an effective solution in helping it build its production and water disposal facilities on budget and in record time: Victaulic’s Refuse-to-Fuse System for high-density polyethylene (HDPE). This solution is helping operators in the Permian construct these facilities in shorter timeframes—on average 9-10 days, compared to 10-12 weeks with the fusion process—and with lower, overall installed costs. The system has been so successful that the company, which typically builds around a dozen produced water disposal facilities per year, has completely switched from fusing to Victaulic’s new HDPE system.

The Victaulic system (Fig. 1) is a line of small- and large-diameter couplings, fittings, transitions and accessories that can join HDPE pipe up to 10 times faster than fusion. The couplings require only commonly used hand tools for assembly, eliminating the need for special equipment and certified crews. The couplings also can be installed rain or shine, without protective tents or covers, and joint completion time does not depend on atmospheric conditions.

Historically pipe-fusing, or fusion, which requires the use of expensive equipment, tools and trained personnel, has been the common method used in water and slurry HDPE lines. However, the Victaulic system eliminates the need for fusion, providing a faster, simpler joining method for the oil drilling and saltwater disposal industry, and can be used in a variety of applications, including flowlines, water transportation, frac ponds, water treatment, saltwater disposal and facility construction.

On average, one disposal facility is needed for every 30 wells on a lease. As oil and gas companies continue to add rigs and enjoy exploration success, they will have to build more production and saltwater disposal facilities. Any delays in constructing these facilities, and having them ready to go when wells come online, can cost producers millions of dollars per day.

To streamline the fabrication and procurement process, and ensure a quick and efficient installation, a CAD-based system is used to produce construction drawings for a step-by-step project plan using HDPE pipe. The pipe system is then pre-cut and assembled for factory-verified joint integrity at a Victaulic facility near the job site. The spools are then delivered to the site for quick installation. Using prefabricated parts—like a giant Lego set—allows for a quicker turnaround and helps reduce overall labor and installation costs.

The system has been deployed successfully in several U.S. onshore oil and gas plays. It also has addressed other challenges associated with the fusion process, such as those faced by Atlas Resources Partners LP at its Hamman saltwater disposal facility in Jacksboro, Texas.

Prior to construction, the contractor knew the project would face challenges associated with joining HDPE piping and construction schedule constraints. The new system and prefabrication options offered a controlled cost option and contracted the completion date for the facility to 10 days, as compared to what would have been six weeks with fusion. The success on the Hamman saltwater disposal project has led Atlas to use HDPE pipe and the joining system on other projects, including other facility buildouts in the Eagle Ford shale. ![]()

- Subsea technology- Corrosion monitoring: From failure to success (February 2024)

- Applying ultra-deep LWD resistivity technology successfully in a SAGD operation (May 2019)

- Adoption of wireless intelligent completions advances (May 2019)

- Majors double down as takeaway crunch eases (April 2019)

- What’s new in well logging and formation evaluation (April 2019)

- Qualification of a 20,000-psi subsea BOP: A collaborative approach (February 2019)