Regional Report: Southeast Asia and Australasia

Hydrocarbon production continues its long decline, while energy demand continues to climb across the diverse Southeast Asia and Australasia region. Offshore and onshore, falling production from mature fields is not being offset by exploration and development. Geology aside, efforts to replace lost production is stymied by a mixed bag that includes politics, bureaucracy and civil unrest. Increasingly, environmental issues absorb resources and confound efforts to improve production.

AUSTRALASIA

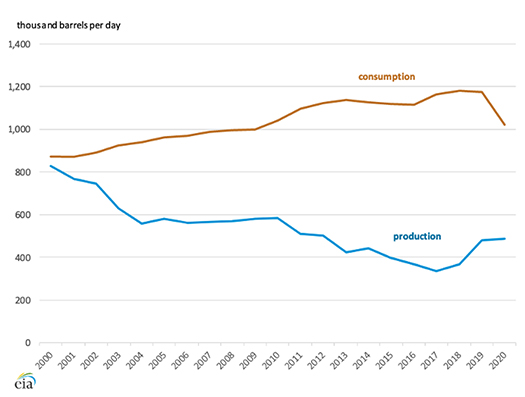

Australian production was 461,000 bopd in 2021, marking an overall decline from a 2000 peak of 828,000 bopd. The country is a net importer of oil, with only around 12% of refinery feedstock produced domestically. The government’s Geoscience Australia (GA) group estimated total 2019 oil production at 131 MMbbl. About two thirds of this was condensate and LPG resources associated with producing gas fields.

Since 2017, Australian production has trended upward, thanks to new projects coming onstream in the North West Shelf region. But there are few new projects being planned—the earliest is the Barossa Project, which Santos expects to come online in 2025. A U.S. Energy Information Administration (EIA) analysis update this year foresees little change in Australia petroleum production through 2023, Fig. 1.

Recent projects include the Northern Carnarvon basin and Browse basin, where there was an 18% gain in oil and condensate production and a 32% increase in natural gas liquids output in 2018, compared with 2017.

The Greater Enfield project in Northern Carnarvon consists of 12 development fields. It started production in 2019, adding approximately 41,000 bopd and reserves of 69 MMboe, according to EIA figures.

The Prelude floating LNG project in the Browse basin started production in 2018. While most of the production is natural gas, it produces 47,600 bcpd and 12,700 bpd of LPG. The basin’s Ichthys field also started production in 2018. It has a production capacity of 48,000 bpd of LPG and 100,000 bcpd.

Future production gains will come from recent expansions to Chevron’s Gorgon Project and Woodside Petroleum’s North West Shelf Project. However, that potential was complicated in October, when Western Australia’s Environmental Protection Authority (EPA) added a requirement for tapering total carbon dioxide emissions to net-zero by 2050.

The change comes with a federal review of mechanisms that cap emissions on the country’s 215 largest industrial and resource emitters. Gorgon has been the largest emitter over the past five years, according to The Sydney Morning Herald. The EPA has also recommended a net-zero requirement for Woodside’s North West Shelf plant and reportedly plans to issue recommendations for Woodside Petroleum’s Pluto and Chevron’s Wheatstone plants.

Gorgon. Chevron’s Gorgon Project is one of the world's largest LNG projects and the largest single resource project in Australia's history. Average daily production in 2020 was 2.1 Bcfg and 15,000 bcpd.

The project’s construction on the Barrow Island nature reserve was originally permitted, because its offshore fields were suitable for carbon dioxide sequestration. While plans called for Gorgon’s carbon capture and storage capabilities to be fully operational last year, they were operating at only 50%. Designed for 4 million tons of CO2 annually, the project stored just 2.1 million tons in 2021. Chevron could face a bill of more than A$100 million, if required to offset all emissions that breached its approval requirements, according to an analysis cited by The Guardian newspaper.

Three Chevron joint ventures offshore Australia were granted greenhouse gas assessment permits, said the company. The blocks include two in the Carnarvon basin, off the northwestern coast of Western Australia, and one in the Bonaparte basin, offshore Northern Territory.

Gorgon Stage 2. Chevron anticipated first gas during third-quarter 2022 from Gorgon Stage 2, sanctioned in 2018. Located on Barrow Island, about 37 mi off the northwestern coast, the project is operated by Chevron Australia and is a joint venture of the Australian subsidiaries of Chevron (47.3%), ExxonMobil (25%), Shell (25%), Osaka Gas (1.25%), Tokyo Gas (1%) and JERA (0.417%).

The project consists of a three-train, 15.6-Mtpa LNG facility and a domestic gas plant, with the capacity to supply Western Australia with 300 terajoules of gas per day. The subsea gathering system is the largest in Australia and key to producing and transporting gas from the Gorgon and Jansz-Io fields to the LNG plant on Barrow Island. The first LNG cargo left Barrow Island in 2016.

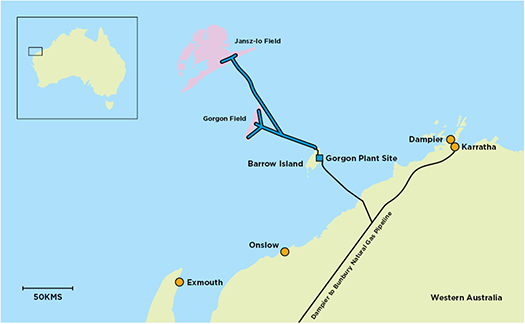

Jansz-Io. The Jansz-Io Compression (J-IC) project, a modification to the existing Gorgon development, was announced in mid-2021, Fig. 2. Chevron says the $4 billion J-IC project is the company’s most significant capital investment in Australia since Gorgon. The J-IC will supply gas to the Gorgon plant from four new Jansz-Io wells and seven new Gorgon wells. Construction and installation activities are estimated to take approximately five years to complete.

“Using world-leading subsea compression technology, J-IC is positioned to maintain gas supply from the Jansz-Io field to the three existing LNG trains and domestic gas plant on Barrow Island,” said Nigel Hearne, Chevron Eurasia Pacific Exploration and Production president. “This will maintain an important source of clean-burning natural gas to customers that will enable energy transitions in countries across the Asia Pacific region.”

The J-IC project will build and install a 27,000-tonne unmanned floating Field Control Station (FCS), approximately 6,500 tonnes of subsea compression infrastructure and a 135-km submarine power cable linked to Barrow Island.

Pluto. Woodside Petroleum began moving gas in March from its Pluto offshore field to the project’s North West Shelf (NWS) LNG plant. A 2-mi pipeline connects the Pluto LNG plant with the project’s Karratha Gas Plant (KGP). The Pluto-KGP Interconnector anticipates future excess capacity at KGP, and it may also help accelerate future developments of other offshore Pluto gas reserves, as well as third-party resources, said Woodside.

Woodside has operated the Pluto facility since 2012. Gas from Pluto and nearby Xena offshore fields is piped to a single onshore LNG processing train, on the Burrup Peninsula near Karratha.

The NWS Project is Western Australia’s largest producer of domestic gas and has provided pipeline gas for more than 30 years. The NWS Project Extension enables long-term processing of third-party gas and fluids and development of existing gas resources, without the need for new processing facilities. Its assets include the KGP, North Rankin Complex (Australia’s largest offshore gas processing facility), and the Goodwyn A and Angel Platforms, Fig. 3.

In response to CO2 emission guidance, Woodside said it has submitted an environmental review document for the NWS Project Extension for approval, to process third party gas and fluid through the existing NWS facility and for the continued operation of the project to 2070.

SOUTHEAST ASIA

Liquids production in Southeast Asia (SEA)has been declining for decades, while natural gas production has been somewhat stable. That trend appears unlikely to change.

Rystad Energy this year predicted that SEA’s combined oil and gas production was unlikely to exceed the 2021 average of 4.86 MMboed in 2021—a 12% drop from 2019—and may decline to 4.3 MMboed within the next three years. Rystad predicted overall hydrocarbon production across SEA would decline an additional 10% by 2025. Key to the drop is declining production from mature fields that make up 60% of the region’s output, as well as difficult regulatory and investment landscapes.

Thailand. In April, Thailand’s national oil company, PTT Exploration and Production (PTTEP), assumed operatorship of the G1/61 project (Erawan, Platong, Satun and Funan fields) and the G2/61 project (Bongkot field), in the Gulf of Thailand. The projects have a combined production capacity of 1,500 MMscfd—about 60% of the nation’s gas supply.

The changes mark the first production-sharing contracts in Thailand’s petroleum history, and they follow 2018’s bidding competition over who would operate the concessions. Chevron, the prior operator of Erawan, also lost its bid to operate the Bongkot concession, where PTTEP continued as operator. Chevron began production from Erawan field in 1981, soon after its discovery of the first natural gas production in the Gulf of Thailand.

At the G1/61 project, operated by Chevron under concession, both parties noted how smoothly the complex handover went, including close collaboration in managing the Erawan 2 and Pattani floating storage and offloading vessels.

PTTEP plans to increase production from G1/61 to 800 MMscfgd by April 2024. The plan includes installing eight wellhead platforms and a subsea pipeline, drilling 183 production wells and adding two drilling rigs for another 52 production wells.

At G2/61, the production objective is 700 MMscfd of natural gas. Initially, PTTEP plans to boost production from Bongkot field, the Arthit project and the MTJDA project, by approximately 125 MMscfgd, 60 MMscfgd, and 30-50 MMscfgd, respectively.

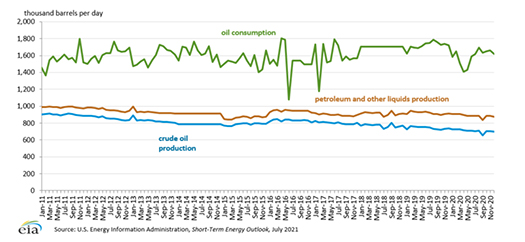

Indonesia. Production in Indonesia fell last year to 858,000 bopd, down from a recent high of 917,000 bopd in 2019, and 895,000 bopd in 2020. Production was 1.013 MMbpd in 2010, according to EIA.

Declining oil production and rising domestic demand present an increasing challenge for Indonesia, says EIA in a 2021 analysis, Fig. 4. Mature fields requiring EOR and, in some cases, basic infrastructure, make up most of Pertamina’s oil reserves, which accounts for about 47% of Indonesia’s production.

An uncertain regulatory environment and government measures have limited foreign investment in extracting these reserves, says EIA. It cites Domestic Market Obligations (DMOs) that funnel at least 25% of oil production to the Indonesian market, as well as disputes with international oil companies have limited Indonesia’s domestic operations.

Indonesia’s reserve replacement ratio in 2018 was only 50%, Deputy Energy and Mineral Resources Minister, Arcandra Tahar, told the Jakarta Post. Lack of technology constrained both exploration and production, he said.

Rokan. Funding for a second phase of efforts to increase production from the Rokan oil block was approved in April by Indonesian regulator SKK Migas. Pertamina took over management of the Rokan block, the country’s second largest producer, in August last year when Chevron’s contract expired. The $2.41 billion investment continues development, aimed at increasing production from 160,000 bopd to 180,000 bopd. Rokan contributes 24% of total national production, Fig. 5.

Pertamina’s Hulu Rokan subsidiary is implementing “massive-aggressive work plans” that include new wells, workovers, water and steam injection technology optimization, chemical enhanced oil recovery (CEOR) technology development and non-conventional oil and gas (MNK). The objectives include drilling an average of one new well per day and shortening the time from drilling to production.

Pertamina said it would ultimately drill 821 wells and upgrade facilities. The program, which will operate at least 20 drilling rigs, had drilled about 130 wells in the first half of 2022. To service the wells, Pertamina said it would grow its current fleet of 29 workover rigs by 36 units. The Rokan Block is one of the largest oil and gas blocks in Indonesia. It includes four main fields—Duri, Minas, Bekasap and Kotabatak—and many smaller ones.

ConocoPhillips closed the sale of its Indonesia assets in the first quarter of 2022. The sale to MedcoEnergi involved a subsidiary with a 54% interest in the Indonesia Corridor Block Production Sharing Contract (PSC) and a 35% shareholding interest in the Transasia Pipeline Company. The sold assets produced about 50 MMboed from reserves of 85 million boe.

Eni began producing gas from the Merakes Project last year. The deepwater gas development is in the East Sepinggan Block, in the Makassar Strait off East Kalimantan, in about 1,500 m of water. Its five deepwater subsea wells are expected to produce 450 MMscfgd. The field is connected to the Jangkrik gas field FPU, and gas travels from there to a liquefaction plant in Bontang, East Kalimantan.

Malaysia produced 611,000 bpd of petroleum and other liquids in 2021, according to EIA, making the country the second–largest oil and natural gas producer in SEA. It is also the fifth–largest exporter of LNG in the world, as of 2019. Malaysia’s national oil and natural gas company, Petroliam Nasional Berhad (Petronas), holds exclusive rights to all oil and natural gas exploration and production projects.

Petronas’ deepwater gas field development off Sabah added a second floating liquefied natural gas (FLNG) facility. The Dua vessel started operations last year in Rotan field, Fig. 6. Capable of reaching gas fields in water depths up to 1,500 m, Dua is expected to produce 1.5 million tonnes of LNG per year. The first FLNG, Satu, is also working offshore Sabah.

Gumusut-Kakap (GK) Phase 3, the deepwater development project off the coast of Sabah, Malaysia, began oil production in July. Two new oil producers and two water injectors were drilled, said Petronas. Once fully completed in Q1 2023, the four wells will add around 25,000 bpd to GK’s existing production capacity.

“The delivery of new production from GK Phase 3 represents yet another milestone in the development of this world-class field, further unlocking its full potential,” said Petronas VP Mohamed Firouz Asnan. "Whilst the shallow inboard areas continue to underpin the country’s production, the future lies in the deepwater plays, which make up a quarter of our offshore acreages.”

Sabah Shell Petroleum is the operator of the GK project, in partnership with Petronas Carigali Sdn Bhd, ConocoPhilips Sabah Limited, PTT Exploration and Production Public Company Limited and PT Pertamina Malaysia Eksplorasi Produksi.

The North Malay Basin (NMB) Phase 3 project produced first gas in September. Located in Block PM302 offshore peninsular Malaysia, Phase 3 was sanctioned in 2019 and includes installation of the new Bergading-B wellhead platform, which adds another 100 MMscfd of gas production, bringing the total production to 400 MMscfgd. It is operated by Hess Exploration and Production Malaysia B.V. (50%), in partnership with Petronas.

Petronas made its third gas discovery in Balingian Province, Block SK411, in shallow waters off the northwest coast of Sarawak. The Hadrah-1 exploration well was drilled to 1,850 m, TD, and encountered gas in a 200-m section of sandstone and carbonate reservoirs.

The success further proves the potential of similar underexplored plays in Balingian province, in Blocks SK411 and SK306, said Petronas. Hadrah-1 is the third 2021 gas discovery in the province. The nearby D18 field also found oil and gas in the same play in 2019.

The Cengkih-1 exploration well discovered gas in Block SK 320 in Central Luconia Province, off the coast of Bintulu, Sarawak. The exploration well was drilled to 1,680 m, TD, in August 2022, encountering a 110-m gas column in Miocene carbonate reservoirs.

The discovery builds on the string of exploration successes in the Central Luconia region. Petronas said the discovery confirms the large potential of carbonate plays in Central Luconia. Development opportunities are enhanced by close proximity of many existing facilities.

Myanmar lastly presents a sad and extreme example of the challenges to regional E&P. The military coup in 2021 and strong international criticism over human rights violations presented such difficulties that majors are leaving the country and its production operations.

Operator TotalEnergies and partner Chevron announced in January this year that they would quit the Yadana Project in the Andaman Sea, which produces natural gas for domestic use and export to Thailand. In July, Thailand’s state-owned PTT took over as operator. In April, PTT and Malaysia’s Petronas also said they would withdraw from Myanmar’s Yetagun gas field, also in the Andaman Sea. WO