Global oil production increases, even as drilling declines further

One of the puniest years in global E&P is occurring during 2016, and there is no clear evidence as to when a discernable upturn will occur. That having been said, the effects of low oil prices have been uneven, geographically, to say the least. North America, in both the U.S. and Canada, has been hit particularly hard. And the situation has been equally bleak over much of South America. So, it was particularly uplifting to see Apache Corporation announce on Sept. 7, that it has hit a massive oil find in far western Texas, despite the depressed market, Fig. 1.

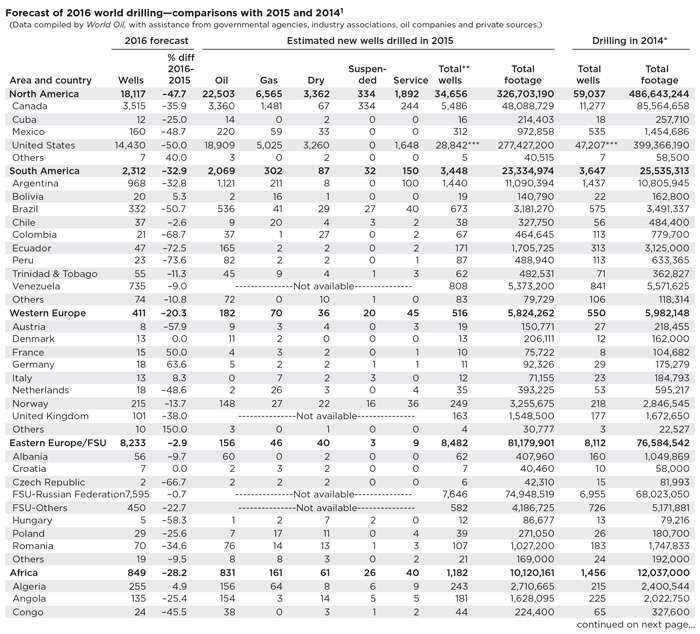

In contrast, the Middle East remains the healthiest E&P region, and there is strength in the Former Soviet Union, principally in Russia, due to that country’s operators drilling furiously to maintain their world-leading oil production rate. On the drilling front, the worldwide total for 2015 was down about 30% from 2014’s level.

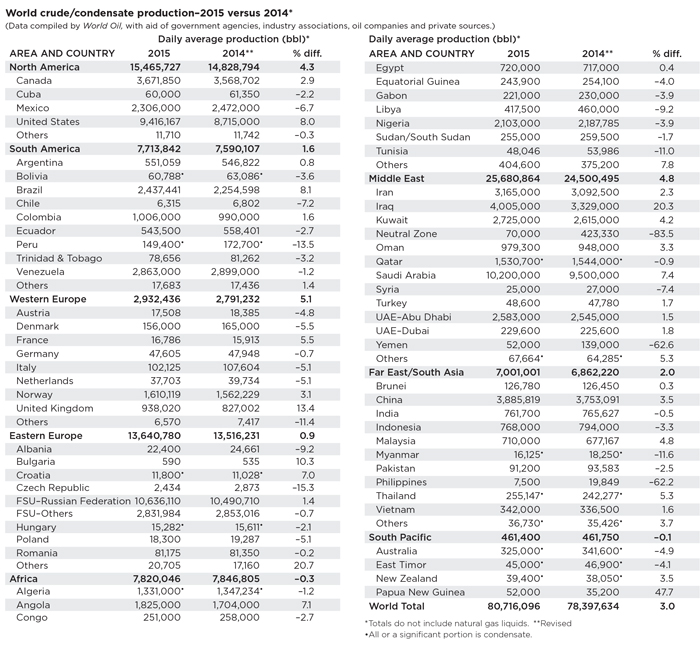

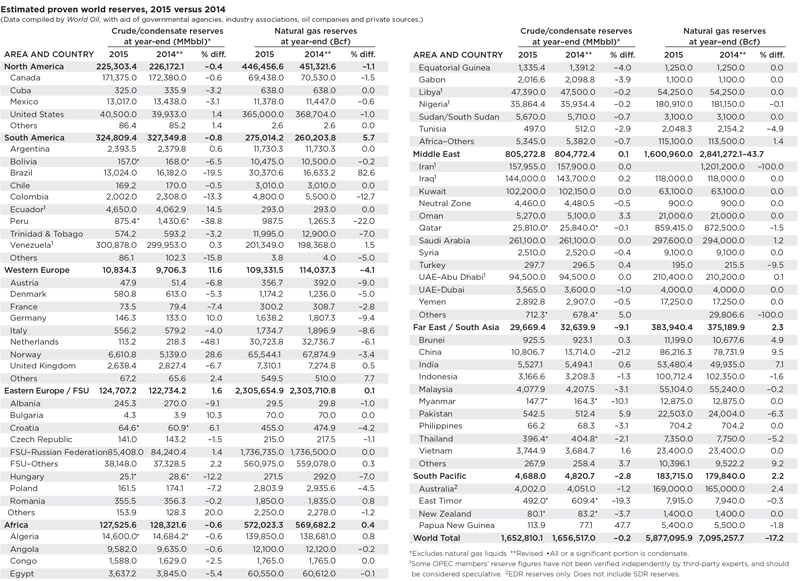

It should surprise no one that oil prices stayed remarkably low through 2015 and well into 2016, given that global crude and condensate production was up an unheard-of 3.0% last year, which compares to historical, average annual gains of 1.0% to 1.5%. Meanwhile, global oil reserves remained flat at 1.653 trillion bbl. Natural gas reserves were up 0.2%, at 7,108.1 Tcf.

Based on these factors and others, we forecast that global drilling will fall 28.5% during 2016, to just 51,008 wells. However, if the U.S. is left out of the equation, then global drilling will be down just 13%. To put this in perspective, the worldwide total is only about 4,000 more wells than what the U.S. drilled by itself two years ago. Some key activity findings include:

- The U.S. will drill a meager 28.2% of wells globally, down from 40.4% last year, and the white-hot rate of 46.5% during 2014.

- For the first time ever, it is possible that China will drill more wells than the U.S. during 2016. We forecast that the world’s top four drilling countries will be, in order, China (15,800 wells); the U.S. (14,430 wells), Russia (7,595 wells) and Canada (3,515 wells). Together, these four nations will drill 41,340 wells, or 81.0% of all drilling, worldwide. This compares to an 82.9% share in 2015, and 86.2% in 2014.

- Russia continued as the world’s top crude and condensate producer last year at 10.64 MMbpd, followed by Saudi Arabia at 10.20 MMbpd. The U.S. again finished third at 9.42 MMbpd, with a gain of about 700,000 bpd (up 8.0%) from the 2014 figure.

- The incredible growth of U.S. oil reserves continued yet again, but the pace has slowed and may stop by the end of 2016. Since its low point of 20.554 Bbbl in 2009, the U.S. number has risen to an official U.S. EIA figure of 39.933 Bbbl at the end of 2014, a 94.3% gain. We estimate that this number grew more slowly last year, to about 40.5 Bbbl.

The following regional assessments give perspective and explanation to the statistical findings.

NORTH AMERICA

Last year saw an incredibly fast contraction in North American drilling activity, as wells drilled fell 41%. This year, we expect a further 47.7% reduction, to just 18,117 wells. Meanwhile, based on gains made from drilling in the 2011-2014 period, regional oil production rose 4.3%, to 15.466 MMbpd.

Canada. Deeply mired in a recession, and with the long-hoped-for recovery still not quite realized, industry observers still think that Canada has hit bottom. The question remains as to how long it will be, before an upturn occurs, although a few bright spots are beginning to show.

Last year, Canadian oil production rose 2.9%, as output averaged 3.672 MMbpd. Oil reserves declined 0.6%, and gas reserves slipped 1.5%. Drilling during 2015 fell 52.4%, to 5,486 wells. This year, we predict a 35.9% drop to 3,515 wells. For more details on Canada, please see World Oil, August 2016, p. 45.

Mexico. Despite its largest discovery in five years, comprising four new fields in shallow water close to giant Cantarell field, Pemex’s E&P activity is still falling. The discovery may have a potential for daily production of at least 200,000 bbl of oil and 170 MMcfg.

As opposed to its disappointing July 2015 license auction, Mexico was more successful with the sale of its onshore fields in December 2015, awarding all 25 licensing contracts to Mexican, Canadian, U.S. and Dutch companies. A deepwater auction is slated for December 2016.

Pemex’s plans for future JVs and higher oil production, however, still have not come to fruition. In fact, like most oil and gas companies, it is simply doing its best to survive the downturn. Overall, Mexican drilling will be down by nearly half this year, production was off 6.7% last year, and reserves declined 3.1%.

U.S. Last year’s precipitous drop in U.S. E&P activity was breathtaking, and this year’s decline will be equally momentous, and certainly historical. During 2015, U.S. drilling totaled just 28,842 wells, down 38.9% from 2014’s level. The single-biggest area of activity left is the Permian basin, where operators are still making money with a break-even price of $37/bbl.

Meanwhile, U.S. oil production was up 8.0%, to 9.416 MMbpd. Oil reserves are estimated to have gained 1.4%, to 40.5 Bbbl. Gas reserves, however, slipped 1.0% to an estimated 365.0 Tcf. For more details on the U.S., see World Oil, August 2016, p. 40.

SOUTH AMERICA

Drilling throughout the region remains in full retreat, as low oil prices continue to wreak havoc on operators’ budgets. South American operators drilled 5.5% fewer wells last year, and they will lower that total another 32.9% this year. Thanks to the prolific drilling that occurred from 2011 through 2014, oil production is still rising in Brazil and Colombia, but the pace is tailing off quickly. These increases were enough to push regional output slightly higher, to 7.71 MMbopd.

Brazil. In 2015, Brazil’s oil output rose 8.1%, to 2.437 MMbpd, according to official figures. The increase stems primarily from pre-salt oil deposits offshore. State firm Petrobras claims that some pre-salt wells are producing in excess of 30,000 bopd, making up a significant portion of Brazil’s total output.

Last year, pre-salt oil production hit a record 865,000 bpd, as new wells came onstream in the Santos basin, the site of multiple oil fields, including Petrobras’ Lula, Jupiter, Libra and Sugar Loaf fields.

The investigation into Petrobras for bribery and money laundering continues in Brazil and the U.S., which has prevented the company from accessing international capital markets. Consequently, the scandal has forced the company to revise its investment plans and conduct a considerable divestment program to raise money.

Scarred by accusations that she had broken budgetary laws to cover losses in the country’s deficit, President Dilma Rousseff lost her impeachment battle and left the presidential palace in Brasilia for good on Sept. 7. She has been succeeded by Michel Temer, the former vice president, who is from a different political party. Thus ends an era of 13 years in power for the leftist Workers’ Party.

Last year, Brazil’s proven oil reserves were revised downward 19.5%, to 13.024 Bbbl. Gas reserves, however, rose a spectacular 82.6%, to 30.37 Tcf. Drilling was up 17% last year, but it is predicted to plummet 50.7% in 2016, to 332 wells.

Venezuela. The country’s oil and gas sector equals about 25% of gross domestic product. Venezuela claims to possess the world’s largest oil reserves, according to its own estimates, but that figure is contested by many independent analysts. Nevertheless, the nation continues to stumble along, earning much of its hard currency as one of the world’s leading oil exporters.

The 23-month downturn in the global oil market has impacted Venezuelan E&P activity heavily. Last year, the country’s oil output declined about 36,000 bpd, to 2.863 MMbpd, and there are thoughts that an even greater decline is in the offing. Drilling was down 4% in 2015, and the outlook for 2016 calls for a 9.0% drop.

Colombia. Despite the many complications of permit delays, rebel attacks on pipelines, community blockades and the theft of seismic data, the country’s upstream sector is prospering from an influx of veteran Venezuelan professionals. These industry veterans fled the oppression of their own country and are now working in Colombia.

Accordingly, Colombian output rose 1.6%, to 1.006 MMbopd. Drilling last year fell 43%, and the outlook this year is for a 69% decline, to just 21 wells.

Even so, Colombia continues to host a sizeable share of the region’s recent discoveries. In August 2015, GeoPark discovered a new light oil field, following the drilling of exploration well Chachalaca-1, on the Llanos 34 Block. And in September 2015, GeoPark reported another oil find in the Llanos basin.

WESTERN EUROPE

Impacted heavily by low oil prices, Western European drilling fell 6.2% during 2015, and a much stiffer reduction of 20.3% is predicted this year. As was the case in 2014, regional oil production rose during 2015, gaining 5.1%, to 2.932 MMbpd.

Norway. As much as any of its neighbors and production rivals, Norway is feeling the sting of continued low oil prices. A number of development projects have been delayed or cancelled, and operators are scurrying to keep their existing fields profitable. According to Norway’s Finance Ministry, overall investment by oil companies is expected to fall at least another 11%.

Nevertheless, some field projects are continuing, as they are too far along to stop. As outlined by Statoil Executive V.P. Tim Dodson, his firm continues to plan for exploitation of the Barents Sea. Dodson said that new, profitable developments will have to come from exploration. “What the industry needs to do is produce high-quality oil from the highest-quality reservoirs,” elaborated Dodson. “And to do that, we need to explore.”

Statoil was awarded five tracts in the Barents Sea last May, as part of Norway’s 23rd Licensing Round. One tract is in the firm’s established position in that area, and the other four are in the southeastern Barents Sea, in the frontier section. Accordingly, Statoil intends to spud its first well in the new area during 2017.

Overall, Norwegian drilling was up 14.2% during 2015, but it will drop 13.7%, this year. Oil production gained 3.1%, to average 1.61 MMbpd. Due to a string of discoveries in recent years, oil reserves jumped 28.6% higher last year.

UK. There is great concern among British officials about how to resuscitate activity in the UK North Sea and adjoining waters. Andy Samuel, chief executive of the relatively new Oil & Gas Authority UK (OGA), has instituted a number of reforms to improve the offshore sector.

“The UK now has one of the more competitive regulatory regimes, and I don’t expect that to change,” said Samuel. “We listened to industry, and we heard from them, that the licensing regime was confusing. So, we’ve been working to improve that.” In the medium term, added Samuel, “improving the seismic data available for the UK is a good thing, and that has to be done.”

One of the things at the heart of the recent Wood Review was a recommendation for more “collaboration” between operators and service companies. “We need to be more like the Norwegian model,” said Samuel. “One area where we’ve seen good collaboration is on technology. We’ve identified five key items in that regard, including asset integrity, well cost reduction small pools, digital and data, and decommissioning.”

Meanwhile, the OGA approved the development of Culzean field in the UK central North Sea in August 2015. The Maersk Oil-operated HPHT field is the region’s largest discovery in a decade, and could potentially meet 5% of total UK demand at peak production by 2020.

British officials and operators have managed to arrest the decline in UK oil production, as output gained 13.4% last year, to average 938,020 bpd. Drilling declined 8% during 2015, and a 38% drop is forecast for 2016.

EASTERN EUROPE/FSU

Throughout the region, drilling last year was up 4.6%, due entirely to a gain in Russian activity, as operators strived to maintain the country’s high oil output. This year, regional drilling will decline about 3%, with only Russia and Croatia remaining roughly even with last year’s pace. At the same time, crude and condensate production, regionwide, rose another 0.9%, at 13.641 MMbpd.

Russia. For a tenth consecutive year, Russia was the world leader for crude and condensate output. Last year, production averaged 10.64 MMbpd (up 1.4%). On the other hand, Russian production of natural gas declined 1.35%, to 58.1 Bcfd.

Oil reserves were up 1.4%, to an estimated 85.4 Bbbl. Gas reserves were flat, totaling 1,736.7 Tcf. Russian drilling was up 9.9% during 2015 (Fig. 2), due mostly to a significant expansion by Rosneft. This year, Russian drilling is forecast to drop less than 1%, to 7,595 wells.

Not all is happy news in the Russian E&P sector. As readers will remember, the conflict between Russia and Ukraine prompted the EU and the U.S. to initiate sanctions against the Russian oil sector. These sanctions have had an onerous impact on Russian oil companies, as well as on their investors. Since Washington imposed the sectoral sanctions, which began in March 2014, the market capitalization of Russia’s highest-ranking oil and gas companies has deteriorated steadily.

Other FSU countries. Wells drilled in former Soviet countries outside of Russia last year were down about 20% at 582. This year, a 22.7% reduction is forecast. Combined oil production from the 14 republics averaged 2.832 MMbpd, down 0.7%. Oil reserves actually gained 2.2%, while gas reserves were up 0.3%.

Within this group, Kazakhstan saw its production dip slightly, from 1.632 MMbopd to 1.626 MMbopd. Azerbaijan averaged 834,331 bopd, down 1.1%. Drilling, both onshore and offshore, totaled 196 wells, down 14%, and coming close to our year-ago prediction of 200 wells. Approximately 175 wells are expected this year.

AFRICA

During 2015, African drilling fell a hefty 19%, due to almost every major country experiencing a decline except Algeria. This year, drilling across the continent is forecast to plunge 28.2%. For a second straight year, African output underperformed, as existing field development projects failed to go onstream, on time, and additional new projects were slowed down or postponed altogether.

Nigeria has its difficulties mount in recent years, particularly concerning its role in the global oil and gas industry. It is the twelfth largest petroleum producer, ranks eighth as an exporter, and has the eleventh-largest proven reserves in the world. Yet, Nigerian production has declined steadily, due to growing underinvestment, as well as ongoing conflict and corruption.

In May 2016, an attack on a JV offshore platform caused Chevron to shut down approximately 90,000 bopd of output. And because of the recent militant attacks, operators are selling onshore and shallow-water oil fields in the Niger Delta region, the country’s foremost oil producing area. Instead, by focusing on deepwater investments, which are farther from militants’ reach, companies hope to minimize disturbances to their Nigerian production.

Looking at recent activity, drilling last year fell about 14%, and the forecast calls for a further 36% reduction. Accordingly, Nigerian oil production shrank 3.9%, to 2.103 MMbpd. Oil reserves were off slightly at 35.9 Bbbl. Gas reserves slipped less than 1%, to 180.9 Tcf.

Angola. As Africa’s second-largest oil producer, Angola saw its output jump 7.1% higher, to average 1.825 MMbpd. Oil reserves remained nearly level at 9.58 Bbbl. Gas reserves also were nearly even at 12 Tcf. Drilling declined 20%, totaling 181 wells. Low oil prices will force a further 25.4% reduction this year to 135 wells.

The first deepwater field to come online was Chevron’s Kuito field (Block 14) in late 1999. In the 17 years since then, IOCs, including Total, Chevron, BP and Exxon Mobil, have put production onstream at additional deepwater fields, and are in the process of developing new ones. Eight additional offshore development projects are expected to come online in the next five to ten years, of which four have relatively firm, estimated completion dates, including Mafumeira Sul (Chevron, 2017); East Hub project (Eni, 2017); Kaombo Project  (Total, 2017) and Cameia (Sonangol, 2018).

Algerian drilling rose 13%, to 243 wells last year, and another 4.9% increase is forecast for 2016. Crude and condensate output was down 1.2%, averaging 1.331 MMbpd. Oil reserves were off slightly at 14.6 Bbbl, while gas reserves climbed 0.8% higher, to 139.9 Tcf.

There has been a dearth of new, major field projects over the last couple of years. The latest significant fields to go onstream were El Merk and Bir Seba. Output began at El Merk in early 2013, and output of crude oil, condensate and LPG averaged about 135,000 bpd in 2015. Bir Seba’s production came online in October 2015, with output of 20,000 bopd that will ramp up to 40,000 bopd by 2020. This new production will only partially compensate for declines in other existing fields.

MIDDLE EAST

The Middle East remains the healthiest E&P region worldwide, due to the steadiness of NOC-operated projects. Even so, drilling will be off slightly this year, losing 1.1% to 3,325 wells. Last year, drilling was up 2.7%. Regional oil production, to no one’s surprise, given the prevailing policy stance in Saudi Arabia, was up a whopping 4.8%, at 25.68 MMbpd.

Saudi Arabia. Production in the Kingdom averaged 10.2 MMbopd during 2015, up 7.4%, and by July of this year, Saudi output had hit an all-time high of 10.67 MMbopd. Meanwhile, oil reserves were steady at 261.1 Bbbl, and gas reserves rose 0.5%, to 297.6 Tcf.

Drilling is estimated to have totaled 617 wells in 2015, a 20.7% gain. A slight increase to 623 wells is on tap for this year. During 2015, Saudi Aramco discovered five new oil and gas fields, raising the total number of discovered oil and gas fields in the Kingdom to 134. The NOC discovered three new oil fields: Faskar, offshore in the Arabian Gulf near e Berri field; Janab, east of Ghawar field; and Maqam, in the eastern Rub’ al-Khali. The firm also discovered two new nonassociated gas fields.

Saudi Aramco also added reserves through delineation drilling, discovering three new gas reservoirs and seven new oil reservoirs in existing fields.

Kuwait. Drilling in the emirate rose again last year, gaining about 17% to 669 wells. This year, we expect activity to remain level. Oil production was up 4.2%, at 2.725 MMbpd. Oil and gas reserves remained essentially flat at 102.20 Bbbl and 63.1 Tcf, respectively.

Kuwait continues in its quest to remain one of the world’s top oil producers, as it pursues a target of 4 MMbpd of crude oil and condensate output by 2020. However, the emirate has had a hard time boosting production for more than a decade, due to upstream project delays and insufficient foreign investment.

UAE-Abu Dhabi. Across the emirate, oil production was up 1.5%. Drilling totaled 222 wells, up 52%. Drilling is forecast to gain another 9.9% this year, totaling 244 wells. Oil reserves remained steady at 94.5 Bbbl, and gas reserves were nearly flat at 210.4 Tcf.

The UAE, as a whole, remains on-track to realize its goal of increasing crude oil production by 800,000 bpd, to 3.5 MMbpd in 2020. And Abu Dhabi is fulfilling its share of that goal, as evidence by the high drilling rate. Thanks to ongoing development, output at Upper Zakum and Lower Zakum fields is increasing to 750,000 bopd and 425,000 bopd, respectively.

Iran. Now that the sanctions imposed on the Iranian oil and gas sector (and other industries) by the U.S. and EU have been lifted, the country is building back its production. And much of the assistance for this work is coming from Chinese firms CNPC and Sinopec. Russian companies are also likely to become increasingly involved. There are estimates that simply restoring oil production to previous levels will require a minimum $150 billion of new investment.

Meanwhile, data compiled by Bloomberg estimated that Iranian oil production was surging after five years of sanctions were ended. According to Bloomberg, Iranian production in early September 2016 was almost at 2011 levels, which would be nearly 4.05 MMbopd. That figure seems a bit high. Overall, Iranian production of crude and condensate rose 2.3% last year. Oil reserves are estimated to have risen 55 MMbbl, to 157.995 Bbbl. Gas reserves were down slightly at 1,201.2 Tcf.

FAR EAST/SOUTH ASIA

Once again, a significant reduction in Chinese drilling during 2015 pushed the region 22.4% lower. This year, a 9.3% decline is on tap. Regional oil production was up 2.0%, at just over 7.0 MMbpd.

China. For a third straight year, Chinese drilling decreased during 2015. Drilling totaled 17,114 wells, down 22%. For 2015, another 7.7% decline to 15,800 wells is forecast. Yet, this total, if our U.S. forecast holds together, will be enough to make China the new, number-one driller. Chinese engineers squeezed out a 3.5% gain in the country’s oil output, for an average of 3.886 MMbpd. On the other hand, officials have revised Chinese oil reserves downward 21.2%, to 10.81 Bbbl.

Upstream projects remain firmly in the hands of the three NOCs: CNPC, Sinopec and CNOOC. New field developments are now concentrated in China’s interior provinces, such as the Northwest’s Xinjiang Uygur Autonomous Region (including the Junggar and Tarim basins) and central Ordos basin (particularly Changqing field). These areas have achieved production growth in recent years through the use of improved drilling and advanced production techniques to tame the complex geology.

India. Wells drilled fell 9% last year, a 4% decline is forecast for 2016. India’s oil production slipped 0.5%, to average 761,700 bpd. Oil reserves were up less than 1%, at 5.53 Bbbl, while gas reserves posted a 7.1% gain.

Indonesian officials say that during 2016, they have managed to stop the decline in oil production. Output reportedly grew for the first time since 2008, with daily output increasing from 768,000 bopd in 2015 to 834,000 bopd in July 2016, an increase of 6.2%. The SKK Migas agency also said that drilling plummeted 56% in 2015, to just 576 wells. That number should shrink another 32%.

SOUTH PACIFIC

Throughout this region (Fig. 3), drilling fell 27%. This year, activity will drop another 41%. Regional production of crude and condensate slipped 0.1%, to about 461,400 bpd.

Australia. Drilling last year dropped 23% higher, with about 40% of the wells drilled offshore. This year, a 42% decline to 109 wells is forecast. Crude and condensate production declined 4.9%, to 325,000 bpd. Oil reserves were down 1.2%, while gas reserves were up 2.4%.

The Australian Petroleum Production & Exploration Association (APPEA) said in early September 2016 that its 2015-2016 data confirm that the country’s oil and gas exploration—onshore and offshore—“is in free fall.” APPEA’s chief executive, Dr. Malcolm Roberts, said, “Over the last two years, spending on onshore and offshore exploration has fallen by almost two-thirds. While some of this fall reflects lower costs, exploration activity is undeniably at its lowest levels for many years. The number of exploration wells drilled offshore is at its lowest level in almost 20 years; onshore drilling is at its lowest level in 15 years.” ![]()