Low oil prices taking toll on Canadian E&P

It was almost exactly six years ago that the Canadian industry faced the kind of bleak outlook that 2015 represents. In this cyclical business, the drivers were different, but the outcomes eerily similar. Consider the following excerpt from the February 2009 issue of World Oil:

“The year ahead promises to provide more stability, but in all the wrong ways. Depressed commodity prices, slumping demand, decreased spending, lower exploration and drilling activity, topped off with massive layoffs, do not provide the type of stability anyone in the oil and gas industry would like to see.”

So, the underlying question is one of structure. In an unstable market, how do producers remain competitive, and position themselves for growth, when the inevitable upswing in oil prices comes? This time, a geopolitical economic war between OPEC—led by Saudi Arabia—and American producers has resulted in collateral damage to the Canadian industry; damage that may prove fatal to some operators.

The only good news, and only for oil and gas exporters, is the decline of the Canadian dollar against the greenback. Recently, the Canadian dollar fell below the 80-U.S.-cent mark for the first time since, you guessed it, 2009. It also has fallen almost 20% in value since early 2013, representing the largest two-year decline on record. Adding to the malaise is a recent cut in interest rates by Canada’s central bank, amid speculation that rates could fall even further as the oil-price slump continues. The upside is that a low Canadian dollar benefits the export-driven oil and gas industry, which ships substantial volumes of oil and gas south to U.S. customers.

Not surprisingly, Canadian producers have slashed budgets and will trim costs wherever possible to help weather the storm. Governments, too—particularly in Alberta—seek to demonstrate fiscal prudence, given the vast reduction in royalty revenues that they have experienced since prices began to fall in mid-2014.

OIL TRANSPORTATION

Amid the broader economic concerns, the focus on market access remains a key priority for both industry, and governments, north of the 49th parallel. Alongside the ongoing Keystone XL soap opera in the U.S., and despite reduced demand for pipeline capacity as less production comes online (or is shut-in), the need for more pipeline capacity out of Alberta remains key to long-term viability of oil supply.

Producers are ambivalent to the destination of their crude, as long as it’s moving to ready buyers. It has become clear that Keystone XL, beyond all hope in Canada, is simply a political issue for the Obama administration, in which any real economic, or business, considerations are irrelevant. So oil is shipped in tankers and rail cars instead, and hopes are pinned to Enbridge’s Northern Gateway project, which will provide access to Asian markets, and TransCanada’s Energy East proposal, which would ship Alberta oil to Saint John, New Brunswick, and then on to offshore markets via Atlantic tankers.

There is the typical opposition to the proposal that pipelines now engender, but in early January, Quebec’s energy board determined that the Energy East project was “desirable,” as it would likely mitigate increased natural gas transportation costs. Regardless, even if it is eventually built, it will be a long time before producers see oil flowing on Energy East.

Meanwhile, opposition to hydraulic fracturing, fed by horror stories propagated among the anti-development fringe of environmental activism, has manifested in significant political attention to the practice, albeit in areas of Canada that have not traditionally had much oil and gas development. New Brunswick, for example, recently imposed a moratorium on hydraulic fracturing. The move is little more than political posturing, as the province has only drilled 80 wells in the last 25 years. Nonetheless, moves like this inevitably generate headlines, regardless of actual impact.

And in Quebec, the provincial environmental review board issued a report, in late December, that concluded that the risks of hydraulic fracturing outweigh the potential benefits. Again, there is little development in Quebec, unlike British Columbia and Alberta, where the practice has been utilized safely for decades.

Political assessments aside, a recent report by Canada’s Fraser Institute on the risks associated with hydraulic fracturing concluded that although more information needs to compiled, the risks associated with the technology are “modest and manageable with existing technologies.”

CAPITAL SPENDING

Given current oil and gas prices, it is hardly surprising that spending plans have been slashed for the upcoming year. In January, the Canadian Association of Petroleum Producers (CAPP) issued a forecast that said spending will fall about one-third this year, compared to last, along with a reduction in oil output growth.

It is expected that drilling will fall substantially in 2015, as well. Early survey returns submitted to World Oil indicated a mixed bag, although many have revised their forecasts downward as the price slump has deepened. Overall, it looks like drilling will mirror spending, falling by approximately one-third this year. Governmental land sale revenues are also expected to fall significantly this year.

With a few exceptions, Canadian producers have announced significant cuts to capital spending in 2015. The country’s largest producer, Canadian Natural Resources Limited, recently announced a 28% reduction in planned spending, to C$6.2 billion, including a reduction of more than 50% in its conventional oil and gas program. The company also revealed plans to reduce spending on thermal oil sands development by almost 60%, to C$460 million, versus the original $1.14 billion announced in November 2014.

Suncor Energy has gone a step further, announcing plans to cut approximately 1,000 employees and contractors, and defer unsanctioned projects in Alberta’s oil sands and offshore Eastern Canada, as part of a C$1-billion reduction in its 2015 capital program. The company’s new program will be $6.2–$6.8 billion, versus its original plans of $7.2–$7.8 billion.

Husky Energy also has slashed spending by one third, to C$3.4 billion from $5.1 billion. Like Suncor, Husky has deferred, by one year, a final decision on its investment to further develop White Rose oil field, offshore Newfoundland.

The only major company that has announced a budget increase this year, Encana Corporation, has stated publicly that it is now revisiting its spending plans, which were based on $70/bbl oil prices. In December, Encana announced plans to increase spending by about 12%, from C$2.5-2.6 billion last year, to between $2.7 billion and $2.9 billion in 2015. However, with oil prices continuing to plunge through January, Encana said that it would review its capital budget and update its spending plans.

A new public entity on the Canadian scene, Seven Generations Energy Ltd., is the lone company on this list that has plans that run counter to the majority, in that it is not reducing its C$1.6-billion capital budget. The company began trading in 2014 after its initial public offering, and has a single active play, the liquids-rich Kakwa River natural gas project in northwestern Alberta.

Crescent Point Energy, meanwhile, has taken the same path as the rest of its peers, announcing a 28% reduction in its capital budget, to C$1.5 billion, from approximately $2 billion. Most of the company’s budget is allocated to its drilling program, in which it expects to drill 616 wells.

Tourmaline Oil Corp. also has cut its spending 13%, to C$1.4 billion, from its previously announced budget of $1.6 billion, reducing its planned number of drilled wells by 30.

M&A ACTIVITY

With instability implicit in the current price environment, mergers and acquisitions (M&A) activity is expected to slow in the short term, but as balance sheets tighten, activity is likely to increase, particularly if the oil price squeeze continues throughout 2015. Access to equity is always constrained in a low-price cycle, and the current environment is no different, so it may also be difficult for companies to access funds from the market to bolster acquisition plans.

As predicted, 2014 saw a substantial increase in mergers and acquisitions, to US$22.5 billion, well ahead of the C$14 billion recorded in 2013, but still substantially less than the C$55 billion in deals during 2012.

Canadian deals in 2014 were highlighted by Spain-based Repsol’s $13-billion bid for Calgary-based Talisman Energy in December. Repsol offered $8/share, plus the assumption of $4.7 billion in debt. Talisman has struggled in recent years with debt levels, and the recent oil-price spiral further exacerbated its tenuous financial position. It was just over a year ago that Talisman was rumored to be the target of France’s GDF Suez, for C$17 billion.

Also in December, EOG Resources announced that it was divesting the majority of its Canadian assets in two transactions, selling its holdings in Western Canada for C$410 million to Tundra Oil & Gas Partnership and Canadian Natural Resources Limited. The assets included 5,800 producing wells over 1.1 million net acres.

DRILLING/PRODUCTION

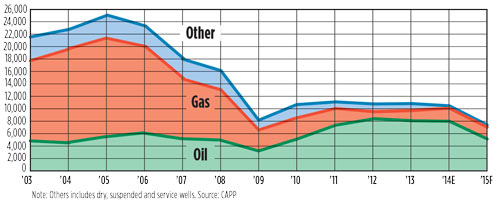

Drilling activity once again targeted oil and predominantly development wells in 2014. According to CAPP records, of the 10,513 wells drilled last year, 76%, or about 8,000, were estimated to be oil wells. Overall, drilling decreased marginally, about 3%, from the 10,878 drilled in 2013. Exploratory drilling fell yet again, down almost 7%.

Canadian producers continue to drill longer wells, with total meters drilled rising to 24.76 million last year, an increase of more than 8% over the 22.80 million m drilled in 2013.

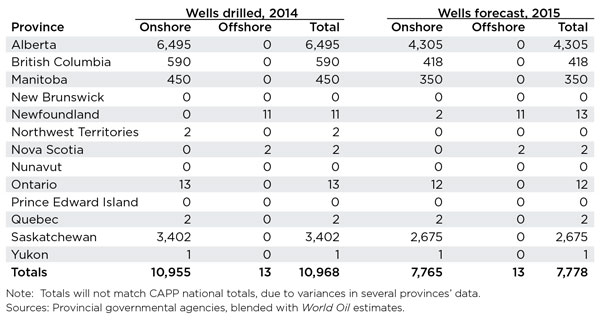

In Alberta, World Oil and provincial data indicate the year-over-year trend of less drilling continued, although the decrease was modest—just over 1.5%—in 2014, with 6,495 wells drilled, compared to 6,598 the year before. To the west, Saskatchewan saw an increase of more than 1% in drilling activity, with 3,402 wells drilled, versus 3,357 in 2013. In British Columbia, the number of wells drilled jumped 8.9% to 590 wells, against 542 in 2013. And in Manitoba, drilling fell 15.9% to 450 wells in 2014, compared to 535 in the previous year.

Looking ahead, the Canadian Association of Oilwell Drilling Contractors is very pessimistic, calling for a massive 43% decrease in drilling activity, to 6,612 wells drilled, with an abysmal average rig fleet utilization of 26%. Meanwhile, the Petroleum Services Association of Canada, although less brutal, is still calling for 7,650 wells in 2015, a decrease of almost 34%. PSAC also noted the intense pressure from producers on service companies to cut prices.

OIL SANDS

When oil prices hovered around $100/bbl, the questions around the extraction of Alberta’s enormous oil sands deposits tended to center on the pace of development, impacts of the massive oil sands mines, new project plans, monitoring of emissions (including greenhouse gases), regulatory oversight and, of course, market access. But with oil below $50/bbl, the conversation has changed. The cost of shipping oil by rail, rather than pipelines, also looms as a significant cost pressure.

Oil sands operators are shelving projects, making layoffs, and looking for cost-savings. None of the players in the oil sands game are going to shift off the long-term view that companies must have to compete and be successful. In fact, several of the larger operators have already stated publicly that they have no intention of reducing production in 2015. But the uncertainty of this price environment is putting further pressure on all of them, and it is also uncertain what impacts a protracted price slump might have on oil sands operators.

In addition, as oil sands production shifts increasingly to in situ recovery, rather than mining, the array of technical options continues to grow, as operators become increasingly innovative in extracting bitumen. Regardless of short-term issues, oil sands production is still expected to reach 3.0 MMbpd before the end of 2015.

Meanwhile, a recent study illustrates the enormous value that the oil sands represent to the Canadian economy, with oil at any price. In November, the Canadian Energy Research Institute estimated that oil sands investments and revenues will add approximately C$3.87 trillion to Canada’s Gross Domestic Product between 2014 and 2038. This projects that total investment in oil sands development will top $514 billion in that time frame.

As testament to the long term, Syncrude Canada applied in January for its Mildred Lake extension project, which would increase the Mildred Lake work area by almost 200%. This would extend the mine’s life by some 14 years, processing an additional 738 MMbbl of bitumen.

LAND SALES

Land sales saw a modest resurgence in 2014, once again surpassing the C$1-billion mark. Overall, bonus revenue reached $1.08 billion, just marginally higher than the previous year’s C$992 million, but still well behind the record $5 billion collected in 2008. The increase comes despite a substantial drop in Alberta land sales, which plummeted 30% to C$494 million, well behind the $698 million seen in 2013.

That decline was offset largely by a massive increase in British Columbian revenue, which rose 70%, to C$383 million, compared to $225 million in 2013. The big increase is attributed to B.C.’s liquids-rich Montney shale, which has revitalized the province’s oil-and-gas sector over the past several years.

In Saskatchewan, revenue also increased substantially over 2013, rising almost 200%, to C$198 million, versus $67 million the year before. Land sale bonus bids fell once again in Saskatchewan, to $67 million, a 37% decrease from $106 million in 2012.

Finally, an East Coast offshore work commitment drew a record C$559-million bid, for rights to an exploration parcel in the Flemish Pass offshore Newfoundland.

Land inventories are a consistent indicator of future drilling activity; the decrease in land sale volumes indicates that although there are some positive signs in Canada, it would be premature to suggest that any big increase is imminent. ![]()

- What's new in production (February 2024)

- Prices and governmental policies combine to stymie Canadian upstream growth (February 2024)

- U.S. operators reduce activity as crude prices plunge (February 2024)

- U.S. producing gas wells increase despite low prices (February 2024)

- U.S. drilling: More of the same expected (February 2024)

- U.S. oil and natural gas production hits record highs (February 2024)