ShaleTech: Marcellus/Utica

The current forecast for the Marcellus/Utica shale calls for continued perplexity. While it is reasonable to assume that operators would be poised to batten down the hatches to ride out stubbornly depressed gas prices, activity in the early going suggests otherwise.

Despite average prices hovering around $3/MMbtu—and with later-than-usual winter withdrawals freezing out the typical seasonal bumps—comparatively low well costs, combined with expanding takeaway capacity into the nation’s largest gas market are, for now, contributing to relatively stable drilling activity. The most recent rig count shows the combined Marcellus and Utica shale activity dropping a single rig, at the same time that double-digit nosedives were being recorded across Texas and elsewhere.

Yet, fresh off another year of record production, inventories chock-full and prices showing no sign of improving anytime soon, it would seem a given that a sizeable pullback would be in the offing across the 95,000-sq-mi combo play that stretches across most of the Appalachian basin of the eastern U.S.

Or not.

On the one hand, unlike most operators, which had not released 2015 capital budgets as of late January, Marcellus/Utica first mover Range Resources twice announced significant 2015 reductions. In December, the Fort Worth, Texas, independent reduced its year-over-year spending 18% to $1.3 billion; in mid-January, Range cut spending another 33% to $870 million, of which 92% will be spent in the Marcellus.

Denver-based PDC Energy and Canada’s Enerplus, likewise, cut capital expenditures dramatically in the Marcellus/Utica. Enerplus, which holds 53,300 net acres in northeastern Pennsylvania, is decreasing its Marcellus spend by almost 45%, to $90 million. PDC plans to slash 2015 spending in the 67,000 net acres it holds in the Utica to $38 million from the $190 million spent last year. PDC says it will idle the lone rig that it is running, once its Cole four-well pad is on production.

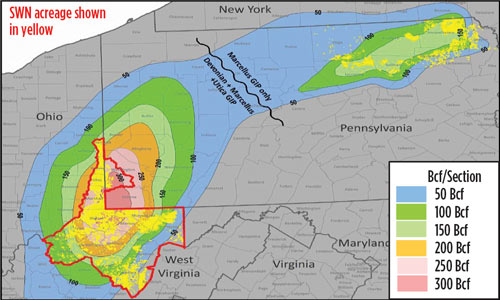

At the opposite end of the spending spectrum is Southwestern Energy. This self-styled contrarian first raised eyebrows with more than $5.3 billion in three back-to-back acquisitions since October, which more than doubled its Marcellus and Utica holdings, Fig. 1. The Houston independent, once more, zigged as its peers zagged, when CEO Steve Mueller told the Houston Chronicle on Dec. 31 that his firm intended to increase capital spending by $200 million, to $2.6 billion this year. “Today’s gas prices are low. We’re a little bit contrarian. We don’t think it will stay in that low $3 range,” he said.

To further justify increased spending, Mueller pointed to its “high economic hurdle” and Southwestern’s projection of a changing tide in the gas supply-demand imbalance. “Supplies are certainly increasing, but the demand growth has matched supply growth since the demand low in mid-2009,” Mueller told investors following the acquisitions. “Almost everyone agrees demand will continue to grow through the end of the decade, mainly driven by new gas power generation and exports, but also including additional industrial growth that takes advantage of the lower energy costs compared to the rest of the world.”

Southwestern, however, is not alone, as both Shale Western E&P (SWEP) and Antero Resources also bolstered their respective footholds recently. In October, SWEP acquired 155,000 net acres in Tioga County, Pa., in a $925-million purchase-and-sale agreement with Ultra Petroleum., which, in turn, acquired SWEP’s interest in Wyoming’s Pinedale field. In January, Denver’s Antero paid $240 million to expand its Ohio Utica holdings by 12,000 acres. Last year, Antero said it put 136 Marcellus and 41 Utica wells online, with average, initial 30-day production of 13.1 MMcfgd/well and 18.5 MMcfgd/well, respectively. As of mid-January, Antero still planned to run an average eight rigs this year.

If current activity is any indication, other operators, likewise, are determined to capture—sooner rather than later—the $90 billion in value that Wood Mackenzie estimates remains in what it tabs “the largest shale gas play in the world.” As of Jan. 22, homegrown EQT said it still intends to operate 12 rigs this year, “and will continue to evaluate that plan, based on economics,” said David Schlosser, executive V.P. of engineering, geology and planning.

As of the week of Jan. 18, an aggregate 124 active rigs were at work in Pennsylvania, West Virginia and Ohio, targeting the often-stacked Marcellus/Utica, down one from the week prior, according to Baker Hughes. A combined 126 rigs were active during the same 2014 reporting period. Of those, 75 were at work in the Marcellus cores of Pennsylvania and West Virginia, which represents a two-rig drop from the previous week. Rigs drilling the Utica, however, were up one from the previous week, with 49 making hole, all but one in Ohio, which remains the epicenter of Utica production. Surprisingly, drilling in the deeper Utica is up 10 rigs from the like 2014 period, according to Baker Hughes.

In the final quarter of 2014, new Marcellus wells dipped to 536 from the 576 wells constructed in the final three months of 2013, Baker Hughes said. The quarterly round-up saw a slight increase in new Utica wells from 112 in the fourth quarter of 2013 to 114 in the same period last year. In both the Marcellus and Utica, the number of wells drilled in the fourth quarter increased over the prior quarter, which recorded 525 and 102 new wells, respectively.

“Looking at the Marcellus, it continues to establish new record levels of production and what we call economy, scale-driven, lower unit cost,” Nicholas DeIuliss, president and CEO of coal and gas operator CONSOL Energy, told analysts at the end of October. “Our E&P operations are posting very strong results in both Marcellus and Utica. This will enable us to continue to drive down operating costs and capital intensity in our business.”

COMINGLED PRODUCTION

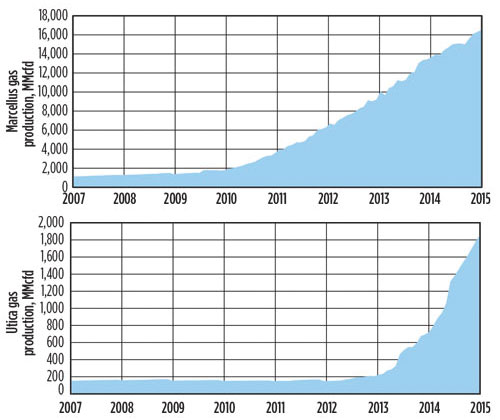

Four years ago, the U.S. Geological Survey (USGS) estimated that the Marcellus shale holds about 84 Tcf of undiscovered and technically recoverable gas, and 3.4 Bbbl of recoverable natural gas liquids (NGLs). A year later, the USGS pegged the Utica with containing an estimated 38 Tcf of gas, about 940 MMbbl of oil, and 208 MMbbl of NGLs. Those assessments helped ignite the onrush of exploration that today has resulted in the record production levels that DeIuliss referenced, which are continuing into the early part of 2015, Fig. 2.

According to the latest tabulations by the U.S. Energy Information Administration (EIA), Marcellus gas production was expected to increase by the end of January to 16.312 Bcfd, up from the 16.009 Bcfd recorded in Dec. The projected month-over month increase is even more dramatic in the Utica, where January production is increased to 1.782 Bcfd, an 85-MMcfd jump over December’s output of 1.696 Bcfd. The more liquids-rich Utica also pumped oil at a 51,638-bpd rate in January, up 4,176 bpd from the 47,462-bpd rate in December. Notably, the EIA said Marcellus gas production for the first time exceeded 15 Bcfd between January and July 2014, the same time period in which Pennsylvania registered record total production of 1.9 Tcf, according to the Pennsylvania Department of Environmental Protection (DEP), the state’s chief regulator.

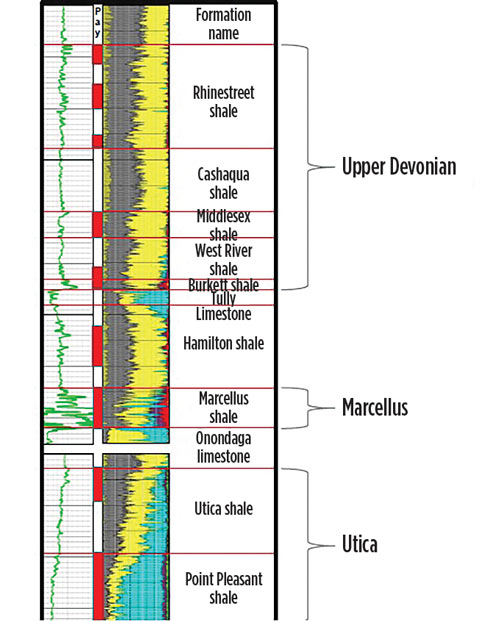

Meanwhile, the “trend du jour” in the Marcellus and the-later developing Utica has more operators capitalizing on the stacked play potential, Fig. 3. The Marcellus, generally described as a highly organic black shale, trapped between limestone strata at depths of 4,000 to 8,500 ft., is being stacked increasingly with its underlying Utica source rock, its well-defined NGL, oil and dry gas components. The Utica underlies the Marcellus by as much as 7,000 ft, and reaches a depth of more than 14,000 ft as it extends eastward. Over the past couple of years, a handful of operators also have begun looking at the overlying Upper Devonian sand and sandstone horizon.

That would include EQT, which is drilling ahead on a 20-well pad, targeting both the Marcellus and the more lightly explored Upper Devonian, where it holds a 170,000-net-acre position, said Schlosser. Schlosser said the Upper Devonian, while shallower, is not as prolific as Marcellus wells, but is an economical play when stacked. “As roads, pads and infrastructure are already being built for Marcellus wells, when we look at adding Upper Devonian wells to a Marcellus pad, it makes a lot of economic sense, because of the shared fixed costs,” he said.

In addition to the Upper Devonian, EQT holds 580,000 net acres prospective for the Marcellus and 400,000 net acres of Utica holdings, where it plans to drill up to five wells this year. Schlosser said the first Utica test well was spudded in the fourth quarter in Greene County, Pa., and a second Utica test well is scheduled this quarter in Wetzel County, W.V. “The Utica is present on much of EQT’s footprint,” Schlosser said. “The dry Utica wells are deeper than the Marcellus wells and, therefore, are more costly, so we’ll need to see how the economics of these wells compare to Marcellus and Upper Devonian wells. We certainly believe the potential opportunity is large, and we are actively exploring it.”

A CLOUDY 2015

One advantage of the Marcellus/Utica is comparatively low well costs. In its August “Marcellus Key Play Analysis,” Wood Mackenzie says drilling and completion costs across the Marcellus typically range from $6 million to $9 million/well. “We’ve been able to realize operational efficiencies in our drilling and completions operations,” said EQT’s Schlosser. “On the drilling side, multi-well pad drilling, along with targeting multiple formations, has allowed us to spread fixed costs over a larger number of wells, which helps us to control costs. On the completions side, longer laterals have allowed us to penetrate more feet of play and, along with reduced cluster spacing, has translated into more economic wells.”

Across its leasehold, Southwestern estimates average 2015 completed well costs of $6.8 million, each, with longer 5,520-ft average laterals and 14 frac stages. Well costs last year averaged roughly $6.4 million/well, but were constructed with shorter average laterals of 4,566 ft and 15.4 completed stages. Southwestern also is holding firm to its 2015 investor guidance, which calls for putting roughly 160 new wells onstream, with production targets of 490 Bcfe to 500 Bcfe for its now 782,000-net-acre leasehold.

Southwestern first expanded its Marcellus/Utica position with October’s $4.98-billion acquisition of 413,000 acres from Chesapeake Energy, located mostly in northern West Virginia. That deal was followed on Dec. 23 by the $394-million purchase-and-sale agreement with Statoil that covers 30,000 net acres in West Virginia and southwestern Pennsylvania. The deal increases Southwestern’s operated working interest in the acquired asset to nearly 73%.

“The Marcellus justified the acquisition, but it only hints at the exciting upside across the acreage position,” Jeff Sherrick, executive V.P. of exploration and business development, told analysts at year-end. “There have been successful tests within both the Utica and the Devonian section on or near our acreage.”

Also in December, Southwestern paid Oklahoma-based WPX Energy $300 million to acquire 46,700 net acres in northeastern Pennsylvania, along with firm transportation commitment for 260 MMcfd. Sherrick said the WPX takeaway component justifies much of the increased spend planned this year. “In northeast Pennsylvania, we plan to invest $790 million to drill and complete 100 to 108 wells. This is approximately $90 million more than we invested in 2014, and is in keeping with our strategy of ramping up production in line with available firm transportation capacity, and is a direct result of the 260 MMcfd of additional firm gas transportation obtained as a result of our recent WPX acquisition.”

As for its new West Virginia asset, Southwestern plans by year-end to increase to four rigs, and drill between 65 to 70 net wells. During 2015, the company says it will focus on both developing its known acreage, and testing new areas and new zones in northeastern Pennsylvania. “We will continue both extending drilling north for the Lower Marcellus in Susquehanna County and also continuing to extend our encouraging tests in the Upper Marcellus in Bradford County, and into Susquehanna County,” Sherrick said.

Meanwhile, after liquidating nearly 25% of its Marcellus/Utica properties, Chesapeake said it will concentrate on developing its remaining northeastern Pennsylvania acreage, where it projects 7% to 10% production growth in 2015. Chesapeake still controls more than 1.2 million acres, where late last year it ran three rigs and connected 23 wells to production, at an average cost of $7 million/well. Elsewhere, third-quarter production from its 1-million-acre Utica asset averaged 86,000 boed, up 27% sequentially. During the latest reporting quarter, Chesapeake operated seven rigs and connected 77 gross wells on its Utica acreage, at an average completed cost of $6.5 million/well.

Cabot Oil & Gas, which last year installed its first 10-well pad, attributes the tight concentration of its 200,000-net-acre leasehold—entirely in Pennsylvania’s prolific Susquehanna County—as helping hold drilling and completion costs at or below $7 million/well. “We’re fortunate that we’re in the sweetest spot in the play,” said Cabot spokesman George Stark. “We’re impressed with how our wells are coming on, and the EUR we’re getting. But, as you can imagine, prices are a big thing for us this year.”

In November, Cabot laid out tentative 2015 plans that called for five rigs, and estimated drilling of 95 to 100 wells, but at the same time hinted at how its final 2015 game plan could shake out upon its release in February. “Reduction in drilling and completion activity in 2015 is predicated on lower anticipated natural gas price realizations throughout Appalachia, as we await the in-service of new takeaway capacity,” Cabot told investors, referring to the long-awaited Constitution pipeline, which is expected to begin service late this year or in early 2016.

The latest data available from Pittsburgh-based CONSOL Energy show its Marcellus assets delivering 30.7 Bcfe in the third quarter, a 76% year-over-year increase. Utica production rose to 6.8 Bcfe, up appreciably from the 0.2 Bcfe recorded in the year-earlier quarter. CONSOL had not disclosed year-end 2014 earnings, or 2015 capital expenditures at press time, but said it expected to exit the year with eight rigs and the drilling of 182 wet and dry Marcellus wells. Its estimated, year-end 2014, drilling schedule and activity overview also includes 33 new Utica and eight Upper Devonian wells. CONSOL, which has sequentially increased lateral lengths to around 8,000 ft, says it also is conducting a number of stacked play projects, accessing up to four prospective horizons from a single pad, Fig. 4.

“We saw that the third-quarter all-in unit costs in the Marcellus were at $2.69/Mcf, and cash costs were $1.58/Mcf,” DeIuliss said. “Those numbers are hard evidence of cash flow generation and strong rates of return.”

CONSOL holds more than 555,000 acres, including the collective 413,639 net acres included in two 50/50 joint ventures signed in 2011. A Marcellus-oriented partnership with Noble Energy covers 345,151 net acres, while a joint Utica development agreement with Hess covers 68,488 acres in eastern Ohio, Fig. 5. The CONSOL-Noble JV also operates the now-public Cone Midstream Partners LP, which it formed last year to develop Marcellus gas gathering and other midstream assets.

Oklahoma’s Gulfport Energy holds 184,000 net acres, where it targets the Utica, and planned to close out the year with the drilling of 85 to 95 gross wells. At the end of the third quarter, Gulfport was running eight rigs and brought 22 gross wells online with net production of 38,123 boed.

Magnum Hunter Resources controls 118,000 acres, primarily in Ohio, where it is actively pursuing a stacked Marcellus/Utica campaign. In a January investor presentation, Magnum Hunter said it expected to record production of 112.1 MMcfed by July, and singled out its Stalder pad in Ohio’s Monroe County, which delivered initial Marcellus/Utica production rates of 32.5 MMcfd.

In its most recent update, Anadarko Petroleum shows third-quarter, net Marcellus production of 534 MMcfd in its 260,000-net-acre leasehold in north-central Pennsylvania. During the quarter, The Woodlands, Texas-based independent operated one rig and spudded six wells.

REDEFINING THE UTICA

Shell says sustained production results from two producing wells on its newly acquired Tioga County acreage effectively extend the geographic boundary of the Utica play beyond its previously delineated southeastern Ohio and western Pennsylvania fairway.

The Gee discovery well, which was drilled more than 100 mi northeast of the nearest Utica producer, flowed back at an initial rate of 11.2 MMcfd and has been online for nearly a year. The well was drilled to 14,500 ft, MD, with a 3,100-ft lateral, and completed with 13 frac stages. The second well, Neal, delivered a peak flowback rate of 26.5 MMcfd. That well was drilled to 15,500 ft, MD, with a 4,200-ft lateral and 16 frac stages. Results are pending on four additional Utica wells, Shell says.

The twin discoveries extend the Utica core into an area where, following the Ultra Petroleum agreement, SWEP now holds 430,000 net acres.

Range Resources, which controls just over 1.9 million acres on which it targets both the Marcellus and Utica, said on Dec. 15 that its newly completed Utica/Point Pleasant well in Washington County, Pa., established a milestone in Utica production. Range said the well delivered an average 24-hr test rate of 59.0 MMcfd, which it claims represents the highest initial production (IP) rate for the Utica and is believed to be a record “for any horizon drilled in the Appalachian basin.”

“We are very excited about the initial test results of our Utica/Point Pleasant well,” President and CEO Jeff Ventura said in a statement that announced the initial 2015 budget cut. “Given our 400,000-net-acre position in the area, coupled with existing well control and 3D seismic, we believe this translates into significant potential. Being able to drill additional Utica wells on the same locations as our Marcellus wells should further enhance our capital efficiency for many years to come.”

TAKEAWAY RELIEF

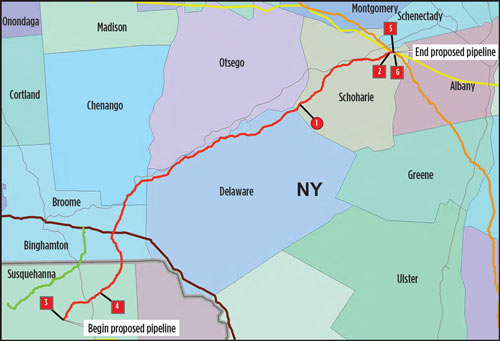

One bright spot, in the otherwise cloudy near-term prospects, is the long-awaited start-up of the Constitution pipeline in late 2015 or first-quarter 2016. Once in service, the network will help ease notorious infrastructure constraints that have long hampered Appalachian producers in moving gas from inventory to burner tips.

In December, the four-company pipeline consortium received the blessing of the U.S. Federal Energy Regulatory Commission (FERC), clearing the way for the estimated 124-mi-long pipeline (Fig. 6) to begin delivering up to 500 MMcfd to the substantial New York gas market. Ironically, the same month that FERC issued its approval for Constitution, the state of New York banned fracing, blocking any development of the Utica, which extends into the state.

Construction is expected to begin this quarter on the 30-in. pipeline that will run from Susquehanna County, Pa. to its termination point in Schoharie County, N.Y. The pipeline is owned by a consortium comprising Williams Partners Operating; Cabot Pipeline Holdings; Piedmont Constitution Pipeline Company; and Capitol Energy Ventures.

“We see ourselves as online and on-time,” says Cabot’s Stark. “It will definitely make a difference, as that’s a huge slug of gas. You have to have the inventory kind of waiting, so when that pipeline opens, you have the gas ready to go into it.”

Constitution is one of no less than 16 takeaway projects in various stages of development with routes stretching into Canada, the Mid-Atlantic and Southeast, as well as the Midwest and Southwest destinations. Once completed, the new networks are expected to deliver incremental takeaway capacity of 25.2 Bcfd. ![]()

- Shale technology: Bayesian variable pressure decline-curve analysis for shale gas wells (March 2024)

- Prices and governmental policies combine to stymie Canadian upstream growth (February 2024)

- U.S. producing gas wells increase despite low prices (February 2024)

- U.S. drilling: More of the same expected (February 2024)

- U.S. oil and natural gas production hits record highs (February 2024)

- U.S. upstream muddles along, with an eye toward 2024 (September 2023)