Regional Report: Eastern Mediterranean

Plans are slowly taking shape to develop what could become a major oil and gas province in the Eastern Mediterranean. Noble Energy’s major gas discoveries, including Tamar and Leviathan fields offshore Israel, and Aphrodite field offshore Cyprus in the Levant basin, have kindled hopes of additional offshore finds along the Levantine coasts of Syria, Lebanon, Israel and the Gaza Strip. Greece and Turkey are also taking advantage of the upsurge of interest in the Eastern Mediterranean region to boost exploration in their waters. In fact, in late 2014, Turkey deployed a seismic survey vessel offshore Cyprus, over blocks that the Cypriot government had already leased to some of the international oil companies, such as Noble Energy, Total and Eni.

UNTAPPED POTENTIAL

The U.S. Geological Survey (USGS) estimated in a 2010 study that the Levant basin formation had mean, probable, undiscovered natural gas resources of 122 Tcf and oil resources of 1.7 Bbbl—estimates that back up the discovery record so far, which suggests that the Levant basin, at least, is predominantly a gas play.

Proved natural gas reserves across all the countries and territories covered in this report amount to around 19 Tcf, most of them in either Israel or Syria, according to EIA data. Virtually all of the 2.5–3.0 Bbbl of oil discovered, so far, lie in onshore acreage in Syria. A host of big name explorers have joined Noble in the region over recent years. France’s Total, Italy’s Eni and South Korea’s Kogas have taken acreage offshore Cyprus, while Royal Dutch Shell, Exxon Mobil and Petrobras are among the firms that Turkey has brought in to further its search for domestic oil and gas resources in the Mediterranean and the Black Sea as it seeks to meet growing domestic energy demand.

These are early days—and the rest of the region has yet to produce discoveries to rival those offshore Israel—but the East Mediterranean’s hydrocarbons potential seems clear. However, rising oil supply from OPEC countries, plummeting oil prices and mounting infrastructure costs may cool the pace of development in the short term. In Israel, government concerns over the dominant position of Noble and its partners in the offshore gas sector is another factor that may slow progress there.

Two years ago, the talk was of developing LNG export facilities in Cyprus and Israel. Meanwhile, in Israel, a floating LNG project, which Noble was considering developing with Australia’s Woodside Petroleum, has been abandoned. Noble is expected to make a decision in March 2015 on whether to pursue an onshore LNG facility in Cyprus. Instead, emphasis has switched to building cheaper pipeline projects to meet gas demand in markets around the Eastern Mediterranean, notably energy hungry Egypt, Jordan and Turkey. Extensions to the existing regional pipeline network have been proposed, such as a route to supply Israeli gas to Turkey. A plan to build a gas pipeline from Cyprus to Egypt also remains on the table.

Another pipeline connection that could be developed in coming months would take gas to Jordan from BG Group’s license area in the waters off the Gaza Strip in the Palestinian Territories. The Jordanian government has said it is poised to sign an agreement to take supply from BG’s Gaza discoveries, as its plans to import Israeli gas have been hit by the slow development pace of Leviathan. Progress with this pipeline will depend heavily on Israel’s attitude toward exports from Gaza, although the Israeli government has said in the past that it would regard them favorably.

Farther north, both Greece and Turkey are eager to attract explorers. Greece has just launched its first offshore licensing round in two decades, while Turkish state-owned energy company TPAO is working with a number of international oil firms offshore in both the Mediterranean and the Black Sea. Meanwhile, Turkey is objecting to the Cypriot government’s leasing of offshore blocks. The chief Turkish negotiator at the island’s reunification talks suggested in late January that Greek and Turkish Cypriots should agree to suspend the search for offshore natural gas until they have reached a settlement to reunify the divided island. Exploration in Syria and Lebanon is on hold, while conflict continues to afflict Syria.

Cost-cutting by oil and gas companies around the world will affect the pace of exploration in the Eastern Mediterranean, as much as anywhere else. In fact, Total has expressed an interest in terminating its lease offshore Cyprus, but has not made a final decision in deference to the wishes of the Cypriot government.

ATTRACTIVE GEOLOGICAL PROSPECTS

The wider Eastern Mediterranean region comprises several basins, of which three have provided the bulk of oil and gas production to date—Nile Delta basin, and Western Arabian and Zagros provinces. The Levant basin has now joined that list of hydrocarbon producers.

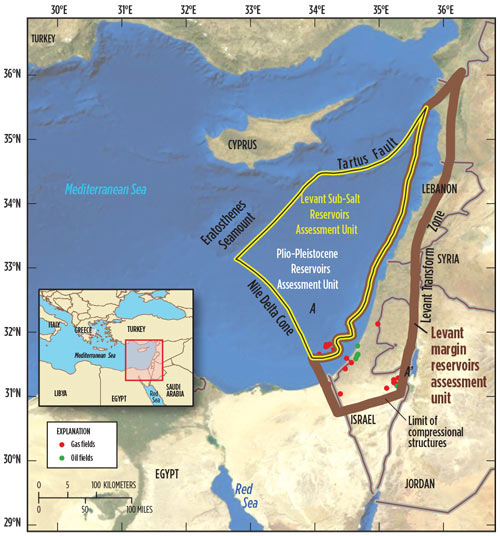

Cyprus’ offshore waters cover a section of the Levant basin and a small part of the Nile Delta basin. Onshore, Israel and Syria straddle the line between the Levant basin and Western Arabian province, which also covers parts of Jordan, Iraq, Saudi Arabia and Turkey, Fig. 1. Some of Syria’s largest fields lie in the Zagros province, which extends from Turkey to the Gulf of Oman, although most of that region’s richest hydrocarbons deposits are in Iraq, Iran and Saudi Arabia.

The offshore Levant basin covers 83,000 sq km, with water depths ranging from 1,500 to 2,000 m. PGS conducted several seismic surveys across part of the Levant basin in 2006-2007, the interpretation of which allowed analogs to be drawn from the proven hydrocarbon-producing provinces of the Nile Delta, northern Sinai, Gaza and Israel. Since then, surveys across a wide swath of the region have been carried out, as interest has grown.

Seismic data suggest that the basin contains up to 10,000 m of Mesozoic and Cenozoic rocks above a rifted Triassic-Lower Jurassic formation. Israel’s large gas discoveries, such as Tamar and Leviathan, are situated in Miocene/Oligocene sub-salt slope and fan sandstones within large anticline structures, of what is known as the Syrian Arc. They are located at total depths greater than 5,000 m.

Noble Energy also has identified Mesozoic oil potential of 3.0 Bbbl at multiple prospects offshore Israel and Cyprus. These are Cretaceous targets in structural and stratigraphic traps, based on strong evidence of a deeper, thermogenic petroleum system. To test these prospects, Noble will have to bring in a rig that could drill 10,000-ft formation depths.

ISRAEL

Some the world’s largest deepwater gas discoveries of recent years have been made offshore Israel, notably in Leviathan field. These could make the country self-sufficient in gas and provide considerable export potential. However, the speed at which they can be developed has been thrown into doubt by opposition to the current ownership structure of Leviathan, and nearby Tamar field, by the country’s competition regulator. There are also concerns over the likely cost of Israeli exports at a time of low oil and gas prices, and abundant hydrocarbons supply from big producers in the adjacent Middle East.

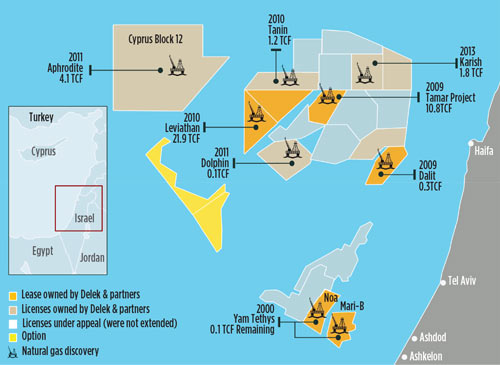

E&P activity. In 2010, Texas-based Noble Energy, and its partner, Delek Group, made Israel’s largest gas find on Leviathan field, some 130 km off the coast in water depths of around 5,000 ft, Fig. 2. Reserve estimates now stand at around 22 Tcf. If Noble’s field development program proceeds as the company has envisaged, commercial production from Leviathan would begin in late 2017 or early 2018, with initial output forecast at around 1.6 Bcfgd. Initial investment in the field is estimated at around $6.5 billion. Noble owns 39.66% of Leviathan, while Delek Drilling and Avner Oil Exploration, both units of Delek Group, hold 22.67% each. Ratio Oil Exploration owns 15%.

The Leviathan find builds on foundations provided by a series of smaller, but still substantial discoveries. The offshore Mari-B field, discovered by Noble and its partners in 2000, provided the backbone of gas supply to the Israeli domestic market—meeting some 40% of demand at one stage—until production fell away sharply in 2012, as it became depleted. That production is now being replaced by output from Tamar field, which was discovered by Noble in 2009. Tamar lies in 5,500 ft of water around 90 km off the coast to the east of Leviathan, and has estimated gas reserves of 10 Tcf. Commercial production there began in April 2013 and averaged 750 MMcfgd during 2013, according to Noble. Existing infrastructure from Mari-B is used to transport and process the gas. By late 2017/early 2018, Tamar is forecast to be producing some 2 Bcfgd.

In 2015, Noble Energy will add production from the newly discovered Tamar SW field, with 700 Bcf gross mean resources and 200 MMcfgd per well. There will be an 8-mi tie-back to the Tamar infrastructure. At Leviathan, Noble has drilled four appraisal wells. An adjacent Karifsh well has 1.8 Tcf of gross mean resources.

Onshore Israel, explorers have had limited success over the years. Afek Oil, an Israeli subsidiary of U.S.-based Genie Energy, says it intends to push ahead in coming months with exploratory oil drilling in the Golan Heights, a highly disputed area annexed from Syria in 1981. Afek has outlined a three-year plan to explore for conventional oil using up to 10 wells, though it has said it may find tight oil, which would be more difficult to extract. Work there has, so far, been delayed by environmental objections. Analysts note that the economics of any project in the region would be open to question in light of low oil prices, while exploration on the border is high-risk. However, political considerations in Israel may help to keep the project moving forward. Another Genie subsidiary, Israel Energy Initiatives, holds a license to explore oil shale reserves in the Shfela basin, in south-central Israel.

Gas sales. On top of supplying the domestic market, Noble and its partners have been seeking gas sales agreements with other countries in the region, including Egypt, Jordan and Turkey. However, uncertainties over ownership of the main fields, due to the competition regulator’s opposition, may slow down or completely stymie deals. So far, only the Palestinian Authority has committed to buying gas from Leviathan, agreeing to a $1.20-billion, 20-year deal.

In early January, Jordan halted talks over a $15-billion deal to supply gas to the kingdom from Israel, citing the monopolies investigation. Opposition politicians in Jordan had also threatened to take legal action in protest over Israeli policy toward Palestine, if gas imports from Israel had gone ahead—more than half of Jordan’s population is of Palestinian origin. Noble and its partners had signed a preliminary agreement, last September, to supply 45 Bcm of gas to Jordan’s National Electric Power Company over 15 years, a deal backed by the U.S. State Department. The partners had also signed a $770-million agreement in February to supply gas to Jordanian-based Arab Potash Company from 2016.

Jordan has said it will now source gas in the short term from BG Group’s operations off the Gaza Strip (see Palestinian Territories section). However, Israel’s National Planning Commission has approved the construction of two pipeline links from Israel to Jordan, which would facilitate Israeli gas supply to Jordan at a later date. Egypt’s oil minister, Sharif Ismael, said in mid-January that the country remained open to the possibility of importing gas from Israel, depending on the development of the Egyptian economy. Egypt used to export gas to Israel, but problems in its own gas industry following the Arab Spring uprising of 2011 and the growth of domestic gas demand mean Egypt is now becoming an importer, rather than an exporter. Delek Drilling has said Israeli exports to Egypt could start by 2017, if an agreement is signed. Turkey is another potential export target for Israel, but plans to build a gas pipeline between the two countries are on hold, following a souring of political relations after hostilities between Israel and Palestinians in the Gaza Strip in 2014.

Exports from Leviathan, using a floating LNG (FLNG) facility to be developed with Woodside Petroleum, were also under consideration initially, but were shelved in 2014 when Noble and Delek opted to focus on supplying regional markets via pipelines, instead. FLNG remains an option for later phases of development, but does not appear to be an attractive option if current global oil market conditions persist, analysts say.

Anti-trust moves. In late December 2014, Israel’s competition commissioner, David Gilo, said the current ownership by Noble Energy and the Delek Group of Leviathan and Tamar fields represented a cartel, and that he would recommend it should be broken up. This reverses a previous decision by Gilo that Noble and Delek could keep control of the country’s two largest fields, if they sold off the smaller discoveries of Karish and Tanin, which have combined reserves of 3 Tcf. This volte-face may reflect growing popular disquiet among Israelis over the role of big business within the country, and the government’s need to assuage such concerns ahead of general elections due in March. If the commissioner’s recommendation is adopted by the government, a lengthy legal case could ensue, while development of the field could be delayed. The decision also could deter further activity in the Israeli energy sector, if companies believe their investments are not safe. Noble Energy has said the decision, if implemented, would affect its investment in Israel, but that it remains ready to develop Leviathan, given the right regulatory, commercial and financial conditions.

CYPRUS

Cyprus became one of the Eastern Mediterranean’s hottest gas exploration targets, when Noble Energy discovered large reserves on Block 12 of the Aphrodite prospect off the island’s south coast in 2011. Total and a consortium of Eni and Kogas have since been awarded exploration blocks in the same region, Fig. 3. Reserve estimates for the discovery, which was made by Noble and its Israeli partners, Delek Drilling and Avner Exploration, were originally put in the 5-8 Tcf range, but have since been whittled down somewhat. Current estimates put reserves at around 4.5 Tcf of gas and 9 MMbbl of condensate in five reservoir sands.

A consortium of Eni and Kogas was awarded Blocks 2, 3 and 9 in 2013. That group drilled its first wells in late 2014, but failed to find significant gas reserves. Total, which has been awarded Blocks 10 and 11, said last year that it intended to drill its first wells in mid-2015. Those blocks lie in water depths of 1,000-2,500 m. In early January 2015, Total indicated a desire to relinquish its leases for lack of suitable drilling prospects. The most likely, initial target for gas would be Cypriot power plants. But, if enough gas can be found, Cyprus wants to build an LNG export plant at Vassilikos to monetize it. The country signed a memorandum with Noble and its partners in 2013 to develop the LNG plant, and has also been discussing the project with the other explorers. However, gas discoveries, so far, are insufficient for the construction of an LNG facility to go ahead.

Possible supply of gas from the Noble-operated Leviathan field in Israel had been mooted to help make the Vassilikos plant viable, but hold-ups in the development of Leviathan and plans to pipe gas from there to other countries in the region, rather than using it for LNG exports (see Israel section), means hopes of taking gas from there anytime soon have faded. The government has remained bullish in public over the onshore LNG development, even if its timetable has slipped. Cyprus National Hydrocarbons Company Chairman Toula Onoufriou said in September 2014 that LNG exports could start by 2022, several years later than originally mooted.

The explorers are less optimistic. John Tomich, general manager of Noble’s Cyprus operation, said in November that high costs and inadequate gas supply made onshore LNG the least attractive export option. Regional pipeline exports looked most attractive, while floating LNG and compressed natural gas options were also being considered, he said. The further fall in global energy prices is only likely to have hardened that view. The outlook is further complicated by continued tensions between Cyprus and Turkey over the destiny of the northern part of the island, which has been occupied by Turkish troops and supported financially by Turkey since a 1974 invasion. The Turkish Cypriot community, backed by Turkey, believes it should take a share of any hydrocarbon revenues, while the Cypriot government insists that revenues should only be shared, once the island is reunified.

Meanwhile, Turkey, which has also lodged claims over some of the island’s offshore acreage, has sent a seismic survey vessel to operate off the coast in waters claimed by Cyprus, a move that caused the Cypriot government to break off peace talks with Turkish Cypriots in October 2014, Fig. 4. Eni and Kogas have been in talks over taking up licenses for Blocks 5 and 6. However, as those blocks lie in waters that Turkey claims as part of its own continental shelf, progress there will be difficult in the near term. If a solution can be found to the northern Cyprus problem, and sufficient gas can be found, the outlook for Cypriot gas could be revolutionized, as that would improve prospects for sending gas by pipeline to the energy-hungry Turkish market. However, such a breakthrough looks unlikely for now. Otherwise, a pipeline to Egypt would seem the most probable export route. To that end, the Cypriot and Egyptian governments said in November that they would enter serious talks over building a pipeline, should enough gas be discovered offshore Cyprus.

PALESTINIAN TERRITORIES

The Gaza strip may be poised to become a gas producer and exporter, after years of uncertainty over whether its reserves could be exploited. Mohammad Hamed, Jordan’s energy minister, said in January, that the kingdom planned to sign an agreement with BG, the operator of the license for all of offshore Gaza, to import gas from the territory via pipeline. The proposed agreement would allow Jordan’s National Electric Power to import 150–180 MMcfgd from Gaza, starting at the end of 2017, and could be signed in first-quarter 2105, Hamed said. The move follows the collapse of talks on the import of gas from Israel’s offshore fields to Jordan (see Israel section).

BG Group has held the exploration license for offshore Gaza since 1999 and drilled two successful wells in 2000—Gaza Marine-1 and Gaza Marine-2, Fig. 5. Resources are estimated to total around 1 Tcf of gas. BG Group holds a 90% stake in the license. This would be cut to 60% if the Consolidated Contractors Company, which owns the other 10%, and the Palestine Investment Fund took up options to increase their stakes, if the block is developed.

In 2002, an outline development plan was approved by the Palestinian Authority for a subsea development and pipeline to an onshore processing terminal. But no concrete progress has been made to date, as BG and the Palestinian Authority have yet to reach agreement with Israel on pipeline exports out of Gaza. Jordan’s announcement suggests that this situation may be about to change. In 2013, prior to last year’s Israeli offensive in Gaza, the Israeli government was reported to be supportive of a Gaza export development.

The Palestinian Authority also has signed an agreement to buy gas from Israel’s Leviathan field, when that project finally goes ahead (see Israel section).

JORDAN

Jordan is keen to find a secure supply of energy, as gas pipeline imports from Egypt are disrupted regularly due to attacks on the pipelines by militants in the Sinai region. The country had been eyeing imports from Israel, but now seems to have put that plan on hold and has, instead, plans to sign an agreement to import gas from BG’s offshore license in Gaza (see Israel and Gaza sections). The kingdom is dependent on imports for oil and gas imports, having very few energy resources of its own. Proved oil reserves stand at around 1 MMbbl, and its proved natural gas reserves are just over 200 Bcf, according to the EIA. Some exploration is taking place close to the Iraqi border and around the Dead Sea. An oil pipeline from Iraq is at the planning stage. The country does have oil shale reserves, which it hopes to exploit. Jordan’s first shale oil-fueled power plant is now scheduled to be operational at the end of 2018.

SYRIA

Production from Syria’s oil reserves, the East Mediterranean region’s largest, has been affected severely by the conflict dominating the country since 2011. Before the war, Syria was producing around 400,000 bopd from proved oil reserves, estimated at 2.5 Bbbl. Now the figure is believed to be well under 25,000 bopd. Gas production has fared a little better. Dry gas production was estimated to have fallen around 30% of pre-crisis levels, to 200 Bcf in 2013, according to the EIA. Natural gas reserves are estimated at 8.5 Tcf. All oil production comes from onshore wells, most of them located in the eastern province of Deir Ezzor, where militant group ISIS now controls much of the output.

Offshore exploration has yet to start, although SoyuzNefteGaz, a Russian firm with close ties to the Kremlin, signed an agreement in December 2013 to start exploring some 2,200 sq km of waters off a 70-km stretch of coast between Tartous and Banias. In 2014, SoyuzNefteGaz’s chairman, Yuri Shafranik, a former Russian energy minister, said exploration would take at least five years to establish the area’s commercial viability, once exploration got underway. No announcement has been made on when exploration will start, and it is unlikely to do so until conflict ends in western Syria.

LEBANON

The hope in Lebanon is that offshore exploration will reveal gas discoveries similar to Leviathan and Tamar fields, across the border in Israel. Drilling success could transform the country’s blighted economy, but plans to push ahead with exploration have been hampered severely by long-term unrest and political volatility both in Lebanon, itself, and in neighboring Syria. A long-running dispute between Israel and Lebanon over the location of their maritime border, which runs close to highly prospective areas of the Levant basin, could also hold back drilling.

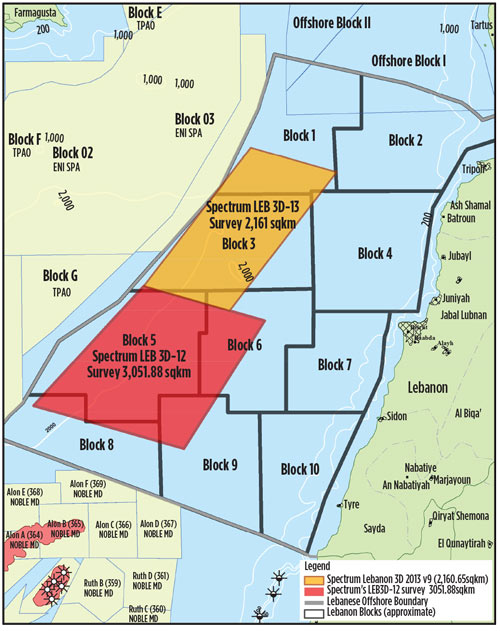

The Lebanese offshore area, known as the Exclusive Economic Zone (EEZ), covers around 22,700 sq km and has been divided into 10 blocks in preparation for licensing. In August 2014, the energy ministry postponed its debut offshore gas exploration licensing round for the fifth time. But the country edged closer to auctioning southern exploration blocks, closest to Israel, after the main political factions reportedly resolved a dispute over who controls them and how they should be licensed. In late December, Prime Minister Tammam Salam told local media that the country’s Petroleum Administration would soon present auction plans to the government for approval.

In recent years, both Petroleum GeoServices (PGS) and Spectrum have carried out 2D and 3D seismic surveys offshore, which reveal four-way dip closure structures, which could be exploration targets, Fig. 6. Meanwhile, in December 2014, NEOS GeoSolutions completed an airborne oil and gas survey covering 6,000 sq km, including the onshore northern part of the country and a transition zone along the coast.

The energy ministry has made offshore gas reserve estimates ranging from 25 Tcf to more than 90 Tcf in recent years, and has estimated that there could be 850 MMbbl of oil. However, a lack of detailed data makes all estimates highly speculative, and the country still faces an uphill battle to persuade international oil companies to invest. For now, in the absence of a regional pipeline network, Lebanon remains reliant on energy imports arriving at its ports on the Mediterranean.

TURKEY

Faced with one of the world’s highest rates of energy demand growth, the Turkish government is operating twin strategies of securing oil and gas imports via pipeline, while trying to speed up oil exploration and production at home, to cut an energy import bill that was rising fast before the recent oil price fall. Turkey produced some 58,000 bopd in 2014, from proved reserves of 290 MMbbl, meeting only a fraction of domestic demand, estimated at some 719 MMbbl, according to the EIA. Most production comes from onshore reserves in the Hakkari basin, in Batman and Adiyaman provinces in the southeast, close to Syria, Iraq and Iran. Some onshore deposits also lie in Thrace, in the northwest. Turkey has discovered virtually no commercial gas reserves, but it consumed around 1.6 Tcf of natural gas in 2013.

Turkey is keen to exploit oil reserves in the Black Sea, which could hold up to 10 Bbbl. Exploration in the Aegean Sea is another target, if boundary disputes with Greece can be overcome. In recent years, there has been an exploration boom in Turkish waters. State-owned energy firm TPAO, which holds preferential rights over all E&P, has brought in Exxon Mobil, Petrobras and Shell, and others to drill, although no major offshore discovery has been made, yet.

Black Sea exploration took another stride forward in early January 2015, with the announcement by TPAO and Shell that the Anglo-Dutch firm had started a $300-million exploration campaign in waters over 2,000 m deep in the western Black Sea, some 100 km offshore from Istanbul. The area is close to where Romania has had drilling success. A drillship has been deployed, following 3D seismic collection. If exploration is successful, a $1-billion investment in a production rig is planned. TPAO and Shell, said the exploratory program was being implemented a year ahead of schedule

On announcing the new campaign, Turkish Energy Minister Taner Yıldız said 45 firms, 17 of the them foreign, had drilled 90 exploration wells and 98 production wells in 2014, and that a third of them had hit oil. He also said that the first seismic survey ship to be built in a Turkish yard would be ready in March 2015. In the Mediterranean, a long-running dispute between Cyprus and Turkey, whose troops occupied northern Cyprus in 1974 and still remain there, threatens to hamper exploration in that region (see Cyprus section). Meanwhile, Turkey has signed various agreements to import oil and gas via pipeline from Russia and central Asia in recent months. This could be augmented by gas supply from Israel’s Leviathan field, if problems surrounding that project can be overcome (see Israel section).

GREECE

Greece launched its first offshore licensing round for nearly two decades in November 2014, following the submission of expressions of interest for blocks offered in August, Fig. 7. The government has been keen to pull investment into its thus-far small oil and gas sector, and has improved fiscal terms and the legal framework for upstream activities, as well as creating an organization, Hellenic Hydrocarbons Resources Management, to oversee the sector. Greece also has indicated that it could reduce tax rates on oil and gas operations in the future. However, the licensing round is taking place at a time of continued economic crisis and high uncertainty in Greek politics, following a change of government in general elections held on Jan. 25, 2015, so the investment climate is far

from settled.

Greece’s oil and gas potential remains relatively under-explored, compared to that of neighbors, such as Albania and Italy. Exploration in the late 1970s and early 1980s by the state energy company led to the discovery of Prinos, Katakolon and Epanomi oil and gas fields in the Aegean Sea. At this time, the only offshore oil and gas production takes place in Prinos field, operated by Energean Oil & Gas. Greece produced just over 7,000 bopd and 180 MMcfgd in 2013, according to EIA.

The new International Licensing Round, only the country’s second, offers 20 offshore blocks in the Ionian Sea off western Greece and to the south of Crete. Following the application deadline on May 14, 2015, the energy ministry is expected to take three months to evaluate bids and then sign lease agreements with successful applicants within the next three months. A data room has been opened containing information from a recent 2D seismic survey carried out by PGS and vintage data. Some 12,350 km of new 2D seismic data were acquired, while around 9,725 km of legacy 2D seismic and 13,000 km of legacy data tied to existing offshore wells were reprocessed. Information for 19 historic wells outside of any currently licensed acreage is also available.

The northern area in the Ionian Sea is an extension of the Southern Adriatic carbonate platform with Late Cretaceous–Eocene carbonates, overlain by a thick Oligocene shale seal and Mio-Pliocene clastics on top. These are analogous to the productive fractured carbonate reservoirs of the central Adriatic to the north, offshore Italy and Albania. In the south, off Crete, the area covered by blocks is in the Ionian zone, analogous to oil fields of onshore Albania, according to the ministry.

The first International Licensing Round took place in 1996, when four concessions were awarded. In 2012, an Open Door Round took place, in which three concessions were awarded. These were Ioannina, which went to a consortium of Energean and Petra Petroleum; Gulf of Patraikos West, awarded to a consortium of Edison, Hellenic and Petroceltic; and finally Katakolon, which was awarded to a consortium of Energean and Trajan Oil and Gas.

DIFFICULT TIMES, BUT HUGE POTENTIAL

As with exploration elsewhere in the world, the oil price collapse of recent months will prompt a strategy re-think for oil and gas firms operating in the Eastern Mediterranean region. Progress in developing Israel’s Leviathan field and associated pipeline infrastructure serving surrounding countries will be watched particularly closely by the industry, as it weighs up further investment in the Levant basin. But an enormous hydrocarbons potential, growing energy demand within the region, itself, and its location close to Europe, and at the heart of international maritime trade routes, should ensure that this oil and gas province has a buoyant future. ![]()

- Advancing offshore decarbonization through electrification of FPSOs (March 2024)

- What's new in production (February 2024)

- Subsea technology- Corrosion monitoring: From failure to success (February 2024)

- U.S. operators reduce activity as crude prices plunge (February 2024)

- U.S. producing gas wells increase despite low prices (February 2024)

- U.S. oil and natural gas production hits record highs (February 2024)