NOVA SCOTIA CANADA: THE NEXT PLAY

Under-explored basins rich with potential

Over 40 Tcf of natural gas is still to be discovered

Schlumberger chairman Andrew Gold, said the age of “easy” oil and gas is over. The Nova Scotia oil and gas industry agrees, and believe his observation bodes well for Nova Scotia’s offshore. Even with a 40-year oil and gas exploration history, Nova Scotia is still a frontier.

Exploring an offshore frontier is akin to putting together a puzzle without knowing what the picture is. Bursts of activity have helped fill in many blanks, but the full picture is far from complete.

Our potential is promising and undeniable. Consider the potential of at least 40 Tcf gas, over an area of more than 400,000 sq. km. Combine that with multiple, untested play types and hundreds of undrilled features, and our future prospects look bright indeed. Add to that the fact that Nova Scotia is within 1,000 km of the largest energy growth market in North America - New England-and we’ve got an excellent combination.

We have seven commercial discoveries, including the Sable Offshore Energy Project, as well as 16 significant discoveries that are undeveloped. We have gas potential in our offshore that industry needs to prove up and develop. Canada-Nova Scotia Offshore Petroleum Board chair Diana Dalton, says there’s no doubt that the province’s offshore has experienced a recent downturn in exploration.

“But rather than being complacent, everyone has to recognize the cyclical nature of offshore exploration, and prepare and encourage the next upturn. As energy prices continue to climb, Nova Scotia will move into an increasingly favorable position. There will be a global rush for new sources of hydrocarbons fuelled by higher prices,” she says. Offshore Nova Scotia consists of three main basins: the Scotian Basin, a portion of the Sydney Basin and the Orpheus Basin.

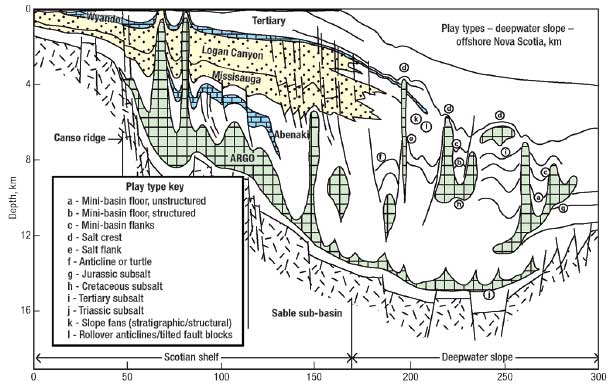

The Scotian Basin comprises a series of combined depotcenters and includes the Sable and Abenaki subbasins, as well as the Shelburne subbasin and Laurentian subbasin. It also includes the Jurassic Carbonate Bank Complex and Deepwater Slope region. Our success, to date, is in the Sable and Abenaki subbasins, as well as along the Jurassic Carbonate Bank complex. Deepwater drilling, while still in its infancy, has had some limited success in the Deepwater Slope region, with strong potential for a major discovery or smaller discoveries in separate fields.

With many untested play types and many hundred identified yet undrilled features, Nova Scotia is encouraging new companies to the offshore with incentives. “We must create winning conditions and new opportunities,” Ms. Dalton says.

In 2001, the Canadian Gas Potential Committee showed 8.9 Tcf of discovered gas in place in the Sable subbasin, while 8.1 Tcf of gas remains undiscovered in this same area. An undiscovered gas potential of 7.1 Tcf was also assigned to the Abenaki subbasin. These numbers are from CNSOPB’s 1997 evaluation.

A large endowment of potential gas, condensate and oil resources has been predicted for the offshore Nova Scotia shelf region and the slope down to the ~5,000-ft isobath.

The last detailed gas resource evaluation was performed by the Geological Survey of Canada (GSC) in 1983 and predicted a mean probability of 18.1 Tcf of gas, 370 MMbbls of associated condensate, and 710 MMbbls of oil.

Analysis indicates that many attractive exploration targets remain in these subbasins and on the Shelf, particularly for gas pools in the range 200 Bcf to 1 Tcf. The report also attributes 1.3 Tcf of risked undiscovered gas potential to the Orpheus Basin.

The Sable subbasin’s Venture Field is an example of excellent reservoir quality in a roll-over anticline. The gas is mostly pooled in overpressured sandstones with a cumulative pay thickness of up to 115 m in some wells. These sandstones, which reach individual thicknesses of 20 m, have permeabilities that range from 0.1-200 mD and porosities in excess of 20%.

Typical gas flowrates from individual zones are 566,000 m3/d (16 MMcfd) with combined test rates from individual wells reaching 2.7 MMm3/d (95 MMcf/d). Similarly, other reservoirs in the vicinity of Sable Island also have excellent porosities and flowrates.

Exploration drilling in the Sable Island area has had some recent disappointments. The Emma N-03 exploration well was a typical example. Drilled in the major Sable Delta complex, the sandstones were wet. Drilling encountered thick reservoir sand sequences in the Cretaceous and Jurassic. Although it had good original porosity, the formation has since been destroyed through void-filling calcite cement and lack of vertical shale, which was unable to produce an adequate seal.

There are still many undrilled opportunities remaining in the Sable Island area. Finding sands is generally not a problem. Listric growth faulting, common in the area, is characteristic of rapid and substantial sediment loading, which is suggestive of a powerful sediment source.

There is added potential in the carbonate bank complex with the Cohasset/Panuke type oil fields. The area is very prospective due to high productivity, shallow water and moderate sea states compared to the deep water. Wells flow at cumulative rates of over 4,610 m3/d (29,000 bpd) of high-quality, 48-52° API oil. Some formations have permeabilities over 2 darcies; individual zones flowed at rates of 1,200 m3/d (7,550 bpd).

The Deep Panuke gas was discovered within the carbonate bank reef complex, which extends 650 km from Sable Island southeast to the offshore US border and beyond. This area is relatively unexplored for these types of oil and gas plays, and great potential exists for more economic development of these field types.

The main gas reservoir is dolomitized, leached limestone reef-margin facies at the top of the thick Baccaro Member. The reservoir has impressive properties: porosities of 3-40%, permabilties of 1 mD to several darcies, and net pay values from 30 m to 100 m. Flowrates have ranged from 50 to 63 MMcfd.

LNG initiatives are proceeding with the Carlyle Group’s 4Gas-led Maple project, as well as the Anadarko project near Port Hawkesbury. Forent Energy is drilling onshore. Stealth Energy is pursuing coalbed methane supply, while Elmworth Energy (Triangle Petroleum Corp.) is pursuing shale gas exploration.

Not all energy activity is related to petroleum. Green energy initiatives are also part of the Nova Scotia energy picture. Tidal power is being pursued on the Bay of Fundy, harnessing the world’s largest tides. Wind and wave energy projects are adding to the stable of renewable energy initiatives being pursued in Nova Scotia.

|