OUTLOOK

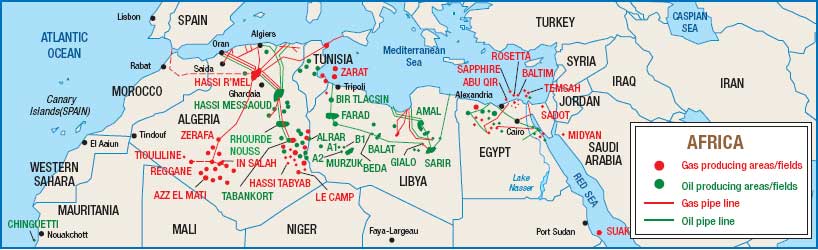

North Africa sees major growth

Production and activity are up in the major countries, with no end in sight.

Gordon Feller, Contributing Feature Writer, North Africa

LIBYA

Libya is well endowed with hydrocarbon resources, and the country has great potential to increase oil and gas production in the future. With relatively modest domestic demand, it also has the potential to increase exports. Libya’s current level of recoverable crude oil reserves is 34.1billion bbl and natural gas reserves are 51.5 Bcf.

The country’s oil production averaged 1.705 million bpd last year, up 3.6% from 2005’s level. The US Energy Information Administration estimates Libyan gas production at about 250 Bcf annually, although government officials in Tripoli have claimed levels twice that high. New wells drilled are averaging about 125 to 130 per year, including several offshore. For a detailed outlook on the country, please see the Libyan feature article on page 17.

EGYPT

With a flurry of recent discoveries, Egypt has revived its status as a petro-state and is now the world’s sixth-largest natural gas exporter. The government is encouraging foreign investment, as gas becomes an ever more important revenue generator. Egypt’s proven gas reserves are estimated to have doubled since 1999. The sector should show marked growth in the next few years, as oil supplies deplete further.

Later this year, gas exports should account for 30% of all production. Egypt recently became the world’s seventh largest LNG exporter. Officials have launched a $10-billion, 20-year strategy that focuses on maximizing the potential of recent gas finds while opening up more areas for exploration. New firms are entering the market, encouraged by recent progress to diminish bureaucracy in the awarding of concessions.

|

Click to View Larger Image

Fig. 1. Various subsea and platform-based field layouts.

|

|

Key facts about Egypt’s upstream include:

- Apache Corp. is the largest US investor.

- Proven gas reserves are 66.8 Tcf, as of 2005, and probable reserves are believed to be 120 Tcf or more.

- Egypt is the world’s 21st largest gas producer.

- Egypt has become the 13th nation to export LNG.

Egypt’s crude oil, petrochemical and LNG exports during 2006 totaled about $10.3 billion, up 33%, according to a Ministry of Petroleum report. Output of crude, condensate and gas rose 13%. Egyptian General Petroleum Corp. (EGPC), owned by the ministry, has increased output 45%, now that el-Hamad oil field is online, producing just over 13,000 bopd.

Among recent news events, four concession contracts were signed in early 2007 for $158 million, plus $24 million in signing bonuses, to drill 23 wells. Agreements cover 9,000 sq km in the Gulf of Suez and Western Desert. They include Petroleum Oil & Gas Corp.(Gulf of Suez), Albaso Egypt Co. (onshore, South Maruit), Sepsa (onshore, South Alamein), and IOEC and LukOil (onshore, Meliha Zone).

A Russian delegation led by Industry and Energy Minister Viktor Khristenko came to Cairo in April 2007. Several memoranda were signed regarding exploration, production and distribution of Egyptian oil and gas. Khristenko’s meeting with Egyptian Petroleum Minister Sameh Fahmy produced an agreement that will see Gazprom help with processing Egyptian gas and then assist in its export.

Fahmy announced six oil and gas finds, split between onshore and offshore. These finds should add 140 million bbl of crude and condensate reserves, and 1.5 Tcf of gas. Western Desert discoveries are the most important, particularly in the Karam 1 and 2 areas. In April 2007, an Eastern Desert find was made by a Chilean company, testing 2,026 bopd. A second find was made by India’s ONGC within a Gulf of Suez concession. It tested 2,979 bopd and 1.5 MMcfgd.

BP will invest as much as $5 billion in Egypt over the next five years, increasing its total investment there to $20 billion. BP will invest the funds into gas exploration and development, including recent finds in the Eastern Delta. After 43 years of operating in Egypt, BP is now responsible for more than 40% of the country’s oil production.

Melrose Resources is expanding its operations by wresting Merlon Petroleum away from rival bidders. Melrose is funding the $265-million acquisition with a loan from Bank of Scotland. Melrose had already worked in partnership with Merlon to develop Nile Delta gas resources. Hindustan Petroleum Corp. Ltd’s JV company, Prize Petroleum, will put in a bid to acquire Devon Energy’s Egyptian assets. Devon operates four oil-producing blocks in Egypt. The blocks are relatively small, with total production of about 7,000-7,500 bopd.

Dana Gas announced a 15-well (10 exploration wells) drilling program for 2007 through its E&P subsidiary, Centurion Energy. Target depths range from 1,000 to 4,000 m. Last December, Fahmy signed a cooperation agreement on oil exploration with Naftogaz Ukrainy Chairman Oleksiy Ivchenko. Total investment will be $30 million to explore a 974-sq-km area in Alam Al-Shawish (Western Desert).

Fahmy, Jordanian Energy and Mineral Resources Minister Khaled Shreidah and Syrian Minister of Petroleum Sufian Al Alawi agreed to the 324-km third phase of the Arab gas pipeline project, to export gas to Syria and boost energy cooperation between the two countries in the area between the Jordanian border and the city of Homs. Petroleum services company Petrojet will build a 100-km, offshore gas pipeline from Al Sheikh Zowayed in northern Sinai to Ashkelon, Israel, for Eastern Mediterranean Gas. It should cost $20 billion.

ALGERIA

Algeria contains an estimated 11.3 billion bbl of proven oil reserves. With recent oil discoveries and exploration plans, proven reserves could rise. Algeria has over 1.5 million sq km of sedimentary basins, mostly onshore. Exploration density is very low, with only eight to nine wildcats per 10,000 sq km, while the international average is 100 per 10,000 sq km. Algerian oil production capacity should climb in coming years, partly because officials plan to increase upstream investment. Algeria’s output goal was 1.5 million bpd of crude in 2006, with an increase to 2.0 million bpd by 2010. Drilling remains around 80 wells annually.

Last October, Algeria’s national assembly voted to return control of reserves to state company Sonatrach, while imposing a special tax on foreign operators. The new law reverses last year’s liberalization measure designed to attract independent companies into the sector. It had given independent operators 70% of reserves that they discovered. Foreign companies will now have to cede a minimum 51% to Sonatrach, which was also given a monopoly over pipeline transportation. The assembly also voted to impose a tax on foreign firms of up to 50% on all profits made on oil sales above $30/bbl. Resorting to international arbitration in disputes with the state was banned.

Among transactions underway, the deadline for submitting bids for the $3-billion Tinrhert gas-to-liquids (GTL) project has been delayed to the end of 2007. Sasol/Chevron, Royal Dutch Shell and PetroSA have pre-qualified to develop gas and oil fields, and build a 65,000-bpd GTL plant at the port of Arzew. Bidding started in April 2005 and was set to end in December 2005. However, it has been delayed, as interested companies have asked for clarification of terms. Tinrhert should take five years to develop, with 25 years of output. The Tinrhert Block has 17 fields, with about 150 Bcm (5.3 Tcf) of sweet gas in place, plus LPG and condensate.

BG Group is entering Algeria as operator of the Hassi Ba Hamou (HBH) Perimeter contract. BG (36.75%) is partnered with Sonatrach (25%) and Gulf Keystone Petroleum (38.25%). BG bought just under half of Gulf Keystone’s original 75% stake. Technical and economic studies carried out with Sonatrach have identified “a significant potential gas resource base within HBH.” The partners will carry out a first exploration/appraisal phase that consists of a 2,000-km 2D seismic acquisition program, plus a 500-km2 3D seismic survey and at least six wells.

The flip side of a $7.5-billion Russo-Algerian arms deal last year seems to be monopoly rights for Russian firms in exploiting Algeria’s Saharan reserves. Gazprom Chairman Alexei Miller accompanied Russian President Vladimir Putin to Algeria in 2006, when plans for Russian weapons shipments were formalized. In return, Russian firms can now strike deals with Sonatrach. “We will help Algeria upgrade its production systems,” said Miller. “They will share with us their priceless experience of liquefaction.” Lukoil also signed a memorandum of understanding with Sonatrach.

First Calgary Petroleums (FCP) reported encouraging appraisal results from Block 405b, where it is gearing up for a $1 billion gas/condensate development. Two wells in the Central Area of Block 405b, referred to as the Central Area Field Complex (CAFC), flowed at a combined 21,303 boed, including 13,161 bpd of liquids and 48.9 MMcfgd.

|

First Calgary Petroleums is likely to combine development of the CAFC and MLE areas in Algeria. Photo courtesy of First Calgary Petroleums.

|

|

To date, in the CAFC and Menzel Ledjmet East (MLE) field, FCP has cased and tested 19 wells with cumulative flowrates exceeding 1.0 Bcfgd and 104,000 bpd of oil and liquids. FCP is moving toward integrating the CAFC project into the MLE development with an aggressive appraisal program throughout 2007. FCP and Sonatrach won regulatory approval to go ahead with a $1.3-billion development of the MLE field. First output is targeted for late 2009.

Italy’s biggest power company, Enel, signed a 15-year agreement with Sonatrach for 2 Bcm of gas/year to pass through the future, 900-km, 8-Bcm GALSI pipeline. Enel already imports 6 Bcm/year from Algeria. India’s state-owned GAIL is negotiating with Algeria for a long-term LNG supply deal of 2.5 million tons to fuel the Ratnagiri power plant. GAIL seeks first supplies in 2009.

TUNISIA

How important is Tunisia to US and European companies that are active in the country?

Apparently quite important, as shown by Pioneer Natural Resources, which recently announced continued success in its program. A third discovery was struck on the Pioneer-operated Jenein Nord Block. Pioneer now plans to develop Jenein Nord, where the first two wells tested at a combined 12,000-plus boed. A successful appraisal on the Adam Block has been put into operation. Production at Adam has increased more than 60%, compared to 2006 levels. Nine additional wells may be drilled over the remainder of 2007. Pioneer has a substantial interest in the Ghadames basin of southern Tunisia, totaling five blocks and 3.9 million acres.

Then there is London-based BG Group (formerly British Gas), which is investing $1 billion into new gas projects. BG is already Tunisia’s largest investor, having spent more than $900 million on E&P, offshore at Miskar, which provides 65% of Tunisia’s natural gas needs, and at Asdrubal, near the coastal town of Sfax. BG plans a $400-million increase at Miskar. Tunisia hopes to increase its gas reserves, provide fuel for Tunisian Electricity & Gas Co. and reduce imports. Officials say that “new, important projects” will be developed in coming months, with a further $600-million investment.

Meanwhile, the Resources division of Petrofac, the oil and gas facilities service provider, is acquiring a 45% interest in the Chergui concession, in exchange for $30 million in cash. Petrofac will operate the concession after acquiring the interest from Tunisian state firm Entreprise Tunisienne D’Activities Petrolieres (ETAP), which holds the other 55%. The government must approve completion of the transaction.

Tunisian drilling, overall, will be roughly equivalent to the 2006 figure at 20 to 22 wells. The country produced more than 90,000 bopd in 2006, up from 75,000 bopd in 2005, said Khaled Becheikh, ETAP’s president and general director, during an energy conference in Ravenna. “We have new discoveries which will add maybe more than 20,000 bopd this year,” added Becheikh. A new gas project in Hasdrubal, being developed with BG, would boost the existing 1.5 Bcm of annual gas output by “about two thirds.”

Tunisia estimates that its oil and gas demand will grow an average 5% annually to 2030, and thus has started seeking new resources abroad to satisfy a growing economy, said Becheikh. “The government has decided to go overseas to renew reserves,” he said. ETAP’s international arm has started evaluating onshore projects in Mauritania, and the firm also has two E&P joint ventures-Numhyd with Algeria’s Sonatrach and Joint Oil with Libya’s NOC.

Becheikh said Tunisia has improved its fiscal regime and introduced PSAs to attract foreign money. Italy’s Eni is its largest foreign partner in oil. BG is the major gas partner. “We are also in discussions with Repsol and Shell,” said Becheikh. But oil and gas companies are nervous about Tunisia. The economy is wanting in a number of areas, particularly the public sector’s continued dominance and the masses of costly red tape. Since becoming a net oil importer in 2000, Tunisia has needed something to offset its dwindling reserves. The answer may be gas.

Another key element for Tunisia may be a proposed 20-30 Bcm/year (2-3 Bcfd) gas pipeline to cross the Sahara desert, linking Nigeria with Algeria and Spain. It could be online in 2015, but only if the three countries involved get their acts together. A feasibility study on the project, variously named Trans-Saharan Gas Pipeline (TSGP) and Nigal, was recently completed and presented to Nigeria and Algeria by consultants at Penspen IPA.The report’s authors judged the project to be technically and economically feasible, with a likely cost of $10 billion, plus an additional $3 billion for upstream infrastructure work in Nigeria. When completed, TSGP would stretch 4,128 km across Africa, through Nigeria, Niger and Algeria, before passing across the Mediterranean.

|