What's new in exploration

The Fayetteville Shale play: An early evaluation

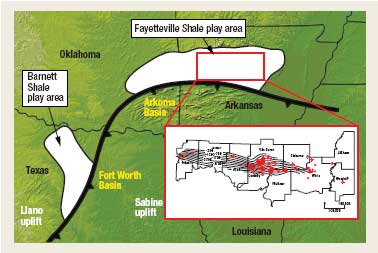

The Fayetteville Shale play: An early evaluation The Fayetteville Shale play in the Arkansas portion of the Arkoma basin is one of the most active natural gas E&P drilling areas in North America. The play is dominated by Southwestern Energy Co., which has drilled 263 wells since 2004, and the company currently produces 155 MMcfgd from the Fayetteville Shale. Other key operators in the play include Chesapeake Energy, Devon Energy, KCS Resources, Yale Oil Associates, XTO Energy and Tepee Petroleum Co. Cumulative production from the Fayetteville is about 29 Bcfg, and per-well reserves on 80-acre spacing are estimated by operators in the play to range 1.3-1.5 Bcfg. Based on data from 187 Fayetteville wells provided by IHS and the Arkansas Oil and Gas Commission, I find little economic justification for the play at present. None of the vertical wells that I analyzed will recover drilling and operational costs. Only 3 of the 136 horizontal wells will be economic in the most-likely case, and only 13 in the optimistic case. Further, I cannot substantiate per-well reserves that approach the levels claimed by operators. The Fayetteville Shale is equivalent in age to the Barnett Shale (Mississippian) of the Fort Worth basin in Texas. Drilling and completion practices established in the Barnett Shale have been applied in the Fayetteville play. These include drilling 3,000-ft horizontal wellbores and using multi-stage, slick-water and cross-linked gel fracture stimulation. Drilling in the Fayetteville has been aggressive. For example, Southwestern Energy has 20 active rigs that drilled 68 wells in the first quarter of 2007, and the company spent $340 million in the play in 2006. While operators have established several pilot areas to evaluate productivity, expectations about drilling results are based largely on faith that Fayetteville production will have similar rates and reserves to those found in the Barnett Shale. Most wells have only a few months of production history on which to predict the outcome of the current drilling campaign. All well and operating costs used in this analysis are based on information from published operator documents. Using a completed well cost of $650,000, a vertical well would have to produce 190 MMcfg at current prices to reach a simple, undiscounted payout value. Of the 49 vertical wells that I studied, 47 have reached their economic limit, and the highest cumulative production is less than 83 MMcfg. Of the two remaining vertical wells, one is projected to be uneconomic (94 MMcf EUR) and the other appears to have been recompleted as a horizontal well and is uneconomic using that cost structure. I performed individual decline analyses for 136 horizontally drilled Fayetteville shale wells using the following averaged data:

Using these cost factors, I developed a simple Net Present Value economic model using a 10% discount rate, optimistic fixed annual LOE and G&A costs, and average wellhead cost for 2006, with the following assumptions, based on decline analysis:

I determined a most-likely EUR by exponentially declining the wells, which is reasonable, considering their very short production histories. I also determined an upside-case EUR by using hyperbolic decline where data permitted, or a most optimistic exponential decline. The model requires an EUR of 850 MMcf for a horizontal Fayetteville well to pay out drilling and operational costs over a three-year production period (plugging costs are not included), a time scale consistent with the economic life for most wells. Using the most-likely case EUR projections, only three wells will reach economic payout (2%). Using the upside-case EUR projections, 13 wells will be economic (10%). Based on well decline analysis, I do not understand the basis for operator claims that an average Fayetteville Shale well will produce 1.3-1.5 Bcfg. In the most likely case, only one well is projected to exceed 1 Bcfg (1.02 Bcfg) and the average value is 341 MMcfg. In the upside case, only six wells will exceed 1 Bcf, and only one well will exceed 1.3 Bcfg (1.5 Bcfg); the average value is 419 MMcfg. Operators hope that the Fayetteville Shale will eventually prove economically similar to the Barnett Shale. While I do not believe that most Barnett wells will be profitable at current gas prices and drilling costs (World Oil, April, June, 2007), I am optimistic that Fayetteville operators will learn how to improve well performance in the play. First, however, they must accept what the data is saying: The Fayetteville

and Barnett shales are different, and evaluation, not continued drilling,

is what is needed. Longer production histories, improved understanding

of how to apply best exploration practices to locate core areas, and different,

more efficient and, therefore, lower-cost drilling and completion procedures

will contribute to a more optimistic outcome for the play. At present,

the outlook is disturbing based on early production histories, and a cautious

approach that does not involve aggressive drilling seems appropriate

and reasonable.

Arthur Berman is a geological consultant specializing in petroleum geology, seismic interpretation and database design and management. He has over 20 years’ working for major oil companies and was editor of the Houston Geological Society’s Bulletin. He earned an MS in geology from the Colorado School of Mines.

|

||||||||