U.S. operators reduce activity as crude prices plunge

Despite escalating tensions in the Middle East, a significant OPEC+ output reduction and the war in Ukraine, crude prices fell in 2023, with WTI down 17.7% to average $77.60/bbl, $16.73/bbl less than the $94.33/bbl average for 2022. During the Covid event and subsequent carbon reduction push, U.S. shale operators remained disciplined with capital expenditures and focused on funneling free cash flow into share buybacks, dividends and debt reduction, rather than drilling new wells.

However, this trend started to change during the second half of 2022, with U.S. activity surging to average 722 rotary rigs during the year. But with U.S. production hitting a record high of 12.93 MMbopd, combined with significantly lower crude prices, U.S. operators responded by pulling back drilling activity in 2023.

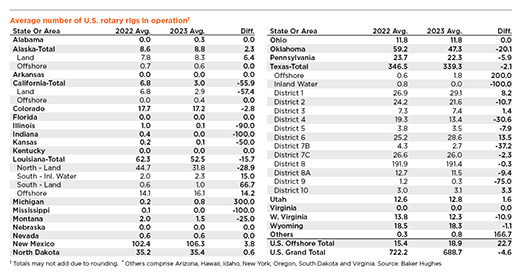

Activity: 2023 versus 2022. The average U.S. rig count for 2023 was 689 units, a 4.6% decrease compared to the previous year’s average of 722. The first week of January, the rig count was 772 and remained above 700 for 20 consecutive weeks before dropping to 696 the week of June 2, 2023. The count declined for 23 consecutive weeks before bottoming at 616 the week of Nov. 10, the low point of the year. Activity recovered during the next seven weeks, ending the year at 622.

Two of the four major oil-producing states enjoyed gains, while two suffered losses in activity. The Texas rig count dropped 2.1%, to average 339 rigs in 2023, with eight of the state’s 12 RRC districts reporting a loss in activity. Despite the overall decline, drilling in the Permian, RRC District 8, was essentially unchanged, down just 0.3% (191 rigs), with RRC District 7C also stable at 26 rigs in 2023 (-2.3%). In the Eagle Ford, oily District 1 was up 8.2%, to average 29 rigs in 2023, two more than in 2022. The gas-dominated portion of the Eagle Ford (District 2) experienced a different fate, suffering an 11% decline, down to a yearly average of 22 rigs, with South Texas District 4 down 31% to 13 rigs.

In gassy Texas RRC District 6, operators working the Haynesville surprisingly upped activity 14% to average 29 wells in 2023. However, drilling in the northern Louisiana portion of the Haynesville plummeted 29% to average 32 wells in 2023. Despite the offsetting scenario, the region’s DUC count increased to 128 wells in December 2023, a jump of 21% on a y-o-y basis, with HH gas price plummeting to average just $2.53/MMbtu, 61% less than the $6.45 MMbtu averaged in 2022.

Despite a nearly 20% drop in the price of WTI, operators in New Mexico upped activity 4% in the southeastern portion of the state, averaging 106 wells in 2023, four more then in 2022. In North Dakota, mature wells are producing more gas than expected and hampering crude output in the Bakken. Despite deteriorating oil output and lower prices, activity in the state was stable, averaging 35 rigs in 2023, the same as in 2022. The discipline to keep drilling activity flat helped decrease the Bakken’s DUC tally 39%, to 323 wells as of December 2023, 208 less than reported for December 2022. Drilling activity in Oklahoma plunged 20%, to average 47 rigs. A 3% decrease was reported in Colorado (17 rigs). Wyoming was down just 1%, to average 18 rigs in 2023.

Offshore. Drilling in Louisiana’s Federal Offshore increased 14% in 2023, to average 16 active rigs, two more than in 2022. In Alaska and California, offshore activity will remain subdued due to unfavorable political climates that has caused operators to reject significant capital projects in those states.

Natural gas regions. In the northeastern U.S., operators working the Marcellus-Utica plays also reduced activity, but at a lower rate than in crude producing regions. Despite the collapse in gas price in 2023, Pennsylvanian was down just 6%, to an average of 22 rigs in 2022, with West Virginia decreasing rig utilization 11% to 12 rigs in 2023. Ohio, which produces more hydrocarbon liquids than its neighbors, was unchanged averaging 12 rigs in 2023 and 2022.

U.S. DUC count drops in oil regions. The deduced activity has caused a significant decline in DUC inventories in oil rich regions during the last 12 months. According to the December 2023 tally by EIA, the overall DUC total stood at 4,374, a reduction of 203 wells since December 2022. However, in the Permian basin operators have completed 239 DUC wells on a y-o-y basis, a reduction of 22% (830 wells). Operators working the Bakken Eagle Ford have managed to slash DUCs in that region 39%, from 531 down to 323 wells. Another significant reduction also occurred in the Eagle Ford play, where producers cut that region’s tally 31%, from 508 DUCs down to 352.

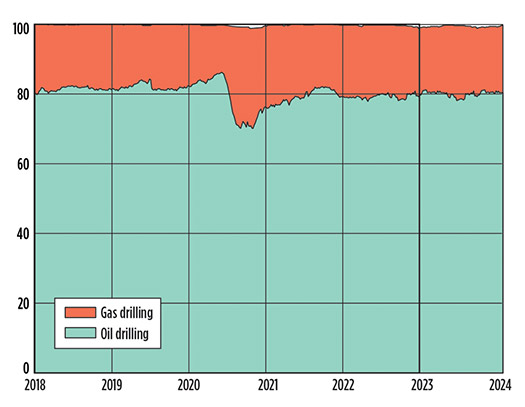

Target split. The HH spot price for natural gas averaged just $2.53/MMBtu in 2023, 61% less than the $6.45/MMBtu averaged in 2022. The massive price drop was due to excessive output of casinghead gas from the U.S. shale plays, especially in the Permian basin. Although the market for U.S. LNG remained strong in 2023, it was not enough to bolster commodity price. Despite an EIA first quarter 2024 forecast of nearly $2.40/MMBtu, HH spot price dropped to $2.01/MMbtu on Feb. 2, and was trading at $1.85/MMbtu at the time of writing.

However, the ratio of rigs targeting gas versus those drilling for crude remained surprisingly steady in 2023, with a few exceptions. In January, approximately 80% of rigs were targeting oil, with 20% drilling for gas. A mild surge in gas drilling occurred during the second half of March and into April, when rigs seeking gas spiked at 22%. For the remainder of the year, the rig seeking gas count versus oil was essentially 20% and 80%, respectively. For reasons unknown, operators in gas dominated regions are electing to continue drilling, then archive the uncompleted boreholes in their DUC inventory, stranding enormous amounts of capital with no ROI in sight. Large year-over-year gains were reported in gas-dominated regions in December 2023. In Appalachia, DUCs are up to 768 (+24%); the Haynesville reported 735 (+21%); and the Niobrara count reached 667 (+27%). These three regions account for 50% of the total U.S. DUC inventory.

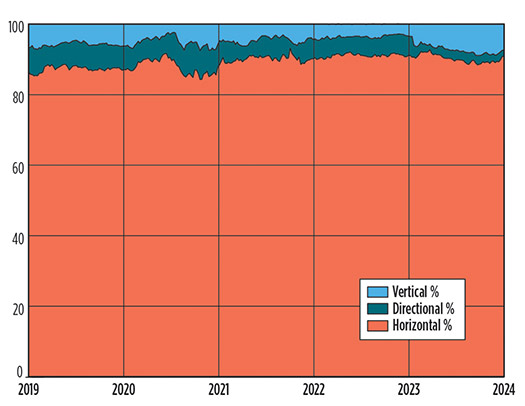

Trajectory split. In 2023, the split between trajectories remained relatively stable throughout the year. Similar to previous years, horizontal drilling accounted for an overwhelming majority of wells drilled. During 2023, approximately 90% of all wells drilled in the U.S. were horizontal, with 7% directional and the remaining 3% categorized as vertical wells.

Related Articles- Coiled tubing drilling’s role in the energy transition (March 2024)

- The last barrel (February 2024)

- Oil and gas in the Capitals (February 2024)

- What's new in production (February 2024)

- First oil (February 2024)

- Digital tool kit enhances real-time decision-making to improve drilling efficiency and performance (February 2024)

- Applying ultra-deep LWD resistivity technology successfully in a SAGD operation (May 2019)

- Adoption of wireless intelligent completions advances (May 2019)

- Majors double down as takeaway crunch eases (April 2019)

- What’s new in well logging and formation evaluation (April 2019)

- Qualification of a 20,000-psi subsea BOP: A collaborative approach (February 2019)

- ConocoPhillips’ Greg Leveille sees rapid trajectory of technical advancement continuing (February 2019)